What tokenized munis actually are

Tokenized municipal bonds are not a new type of security. They are the same debt instruments you already know, but represented digitally on a blockchain. Think of it like moving from a paper deed to a digital title for a house: the asset doesn't change, but the way ownership is recorded and transferred does.

Traditionally, municipal bonds—debt securities issued by states, cities, and counties to fund public obligations—are settled through complex, multi-layered clearinghouses. Tokenization replaces parts of that legacy infrastructure with a distributed ledger. Each token represents a fractional share of the underlying bond, and ownership is immutably recorded on-chain Investor.gov.

This distinction matters because it separates the asset from the rail. The bond still pays interest based on the issuer's creditworthiness and tax status. The tokenization layer simply handles settlement, custody, and transfer efficiency. It is an upgrade to the plumbing, not the product itself.

By keeping the underlying debt instrument intact, regulators can apply existing frameworks to these digital assets. The innovation lies in how quickly and transparently those assets can be traded, audited, and settled, reducing the friction that has long plagued fixed-income markets.

Why infrastructure needs onchain rails

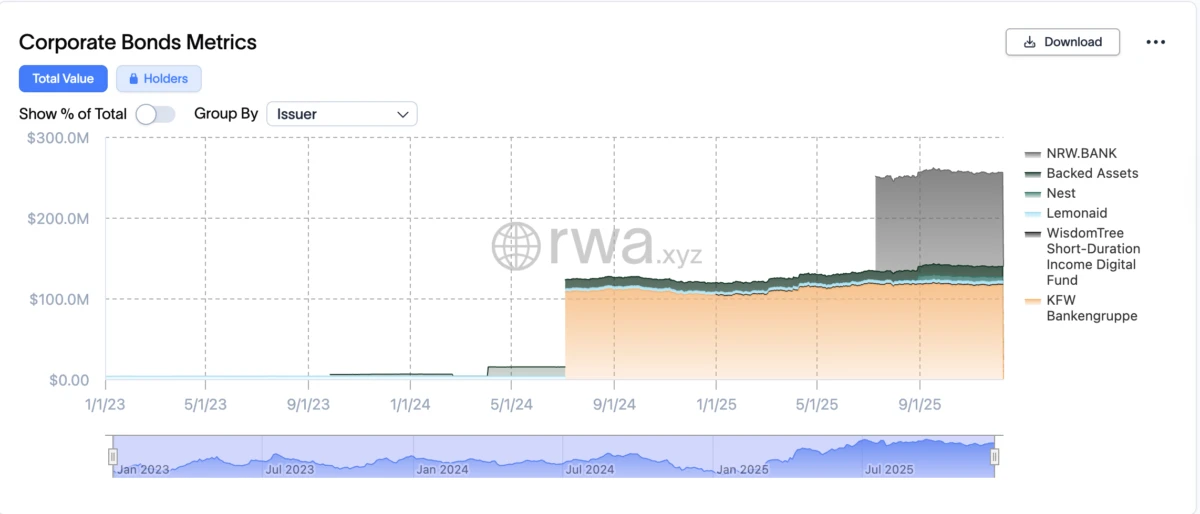

Traditional municipal bond markets have long been plagued by friction. Settlement times stretch over days, and the middleman-heavy structure creates high overhead for both issuers and investors. Tokenized US municipal bonds replace this legacy infrastructure with onchain rails that automate the lifecycle of the debt instrument. This shift isn't just about digitization; it's about fundamentally restructuring how capital flows into public projects.

The most immediate benefit is liquidity. Municipal bonds are typically illiquid, held until maturity by institutional investors who cannot easily exit positions. By tokenizing these assets, ownership is represented by digital tokens on a blockchain, allowing for near-instant settlement and secondary market trading. This transforms a static asset into a liquid one, enabling local governments to raise capital more efficiently and investors to manage risk with greater flexibility.

Fractionalization is the second pillar of this value proposition. Historically, investing in municipal bonds required substantial capital, locking out smaller investors. Onchain tokenization allows bonds to be split into smaller, affordable units. This democratizes access to municipal debt, broadening the investor base and potentially lowering the cost of borrowing for infrastructure projects like schools, roads, and utilities.

Finally, automated compliance ensures regulatory adherence without manual intervention. Smart contracts—self-executing code stored on the blockchain—can enforce investor eligibility rules, such as accreditation status or geographic restrictions, in real time. This reduces the risk of non-compliance and lowers administrative costs, making the entire process more transparent and secure for all parties involved.

How the SEC oversees tokenized municipal bonds

The Securities and Exchange Commission (SEC) is not waiting for the tokenization market to mature before enforcing rules. Regulators are actively applying existing securities laws to digital assets, meaning tokenized municipal bonds are subject to the same rigorous compliance standards as traditional paper bonds. The primary concern is investor protection and market integrity, not the underlying technology itself.

To navigate this complex landscape without stifling innovation, the SEC has developed a regulatory sandbox framework. This approach allows firms to test tokenized municipal instruments in a controlled environment. According to SEC documentation on market modernization, these sandboxes are designed to address specific challenges, such as how investors exchange one tokenized municipal bond for another when those securities exist on different distributed ledgers [src-serp-1]. This controlled testing ensures that interoperability and settlement mechanisms meet federal standards before full-scale public deployment.

For investors, this regulatory clarity is a double-edged sword. It reduces the risk of fraud and operational failure but adds layers of compliance that traditional bondholders do not face. Understanding these oversight mechanisms is essential before allocating capital to tokenized infrastructure projects.

To understand the broader market context, it helps to look at how traditional municipal bond volatility behaves. The chart below shows the performance of the iShares National Muni Bond ETF (MUB), providing a baseline for the asset class that tokenization aims to modernize.

Traditional vs. Tokenized Municipal Bond Structures

Choosing between traditional and tokenized municipal bonds comes down to how you value speed, cost, and access. Traditional munis rely on a legacy clearinghouse system that moves money and ownership records through multiple intermediaries. Tokenized bonds use blockchain technology to record ownership and settle trades directly between parties.

The difference is most visible in settlement times. Traditional municipal bonds typically settle in T+2 days, meaning two business days after the trade date. Tokenized bonds can settle in minutes or even seconds, depending on the blockchain network and the specific protocol used. This speed reduces counterparty risk and frees up capital faster.

Costs also differ significantly. Traditional structures involve underwriting fees, trustee fees, and clearing fees that can add up, especially for smaller investors. Tokenized bonds often have lower transaction costs because they remove or reduce the need for middlemen. However, investors should be aware of potential blockchain network fees and platform charges.

Accessibility is another key factor. Traditional munis often have high minimum investment thresholds, sometimes requiring $5,000 or more per bond. Tokenized bonds can be fractionalized, allowing investors to buy smaller amounts, making municipal bonds more accessible to a broader range of participants.

| Feature | Traditional Muni | Tokenized Muni |

|---|---|---|

| Settlement Time | T+2 Business Days | Minutes to Seconds |

| Minimum Investment | $5,000+ per bond | Fractional amounts possible |

| Transaction Costs | Underwriting, trustee, clearing fees | Lower platform/network fees |

| Liquidity | Secondary market via dealers | Potential 24/7 trading |

| Record Keeping | Centralized clearinghouse | Blockchain ledger |

While tokenized bonds offer efficiency gains, traditional munis remain the standard for large institutional investors who value established regulatory frameworks and deep liquidity in the secondary market. Tokenization is still evolving, with regulatory clarity and market depth developing over time. Investors should weigh these structural differences against their specific goals for yield, risk, and liquidity.

Track performance with live data

You can see how tokenized US municipal bonds are moving in real time. The market for these assets is still developing, so relying on live data is better than reading old reports. Use the widget below to watch the VanEck Municipal Bond ETF (MUB) as a proxy for broader muni market health.

For deeper analysis, look at the daily price action. Tokenized bonds often track their underlying municipal debt closely, but smart contract fees and liquidity gaps can cause small divergences. Watching the chart helps you spot when the token price drifts from the bond's net asset value.

Checklist for evaluating onchain credit

Tokenized municipal bonds bridge two distinct worlds: traditional public finance and decentralized ledger technology. Before allocating capital, you must verify that the digital wrapper faithfully represents the underlying legal obligation. This workflow prioritizes regulatory compliance, technical security, and issuer transparency.

Tokenized securities remain subject to federal securities laws. Confirm the offering has proper registration or qualifies for an exemption, such as Regulation D or the SEC’s sandbox initiatives. Do not proceed if the issuer cannot provide a clear legal opinion on the token’s status as a security. Check the SEC’s EDGAR database for filings.

Code is law only if it is bug-free. Require a public audit from a reputable firm specializing in financial smart contracts. Look for audits that specifically address token transfers, custody mechanisms, and compliance filters. An unaudited contract is an unacceptable risk for any fixed-income instrument.

The blockchain must reflect the actual ledger. Verify that the token supply matches the outstanding principal of the municipal bond. The issuer or trustee should provide regular attestations that the digital tokens are fully backed by the real-world asset. Any discrepancy in supply indicates a broken link between the physical and digital realms.

Tokenization does not change the borrower’s ability to pay. Analyze the municipality’s debt service coverage ratio, tax base stability, and general fund balance. Use tools like the TechnicalChart widget to compare historical yield spreads against the issuer’s credit rating. If the traditional bond market doubts the issuer, the tokenized version carries the same risk.

Municipal bonds are often illiquid by design. Determine if the tokenized version allows for secondary trading or if it is strictly held to maturity. Review the smart contract for transfer restrictions, such as investor accreditation checks or holding periods. A token that cannot be sold when needed offers no liquidity premium.

Frequently asked questions about tokenized munis

How do tokenized bonds work? Tokenized bonds are digital representations of traditional bond instruments on a blockchain or distributed ledger. Instead of issuing a paper certificate, ownership is represented by digital tokens minted on-chain. Each token represents a fractional share of the underlying debt instrument, and its ownership is immutably recorded on the blockchain ledger, allowing for faster settlement and transfer compared to traditional systems.

Are tokenized municipal bonds regulated? Yes. The U.S. Securities and Exchange Commission (SEC) treats tokenized securities as securities under existing federal laws. The SEC has established regulatory sandboxes to test these instruments, ensuring that the digital tokens comply with investor protection standards. Investors must use platforms that adhere to SEC guidelines, including Know Your Customer (KYC) and Anti-Money Laundering (AML) checks.

Can I trade tokenized munis for other assets? Interoperability remains a technical challenge. According to SEC sandbox frameworks, exchanging one tokenized municipal bond for another is complex if the securities exist on different distributed ledgers. Currently, most trading occurs within specific blockchain ecosystems. Investors should verify which networks their chosen tokens support before purchasing.

How does this fit into a 60/40 portfolio? A 60/40 portfolio allocates 60% to equities and 40% to bonds, aiming to balance growth potential with income and stability. Tokenized munis can serve as the fixed-income component, offering liquidity and fractional access. However, they do not replace the need for broad diversification. Warren Buffett’s approach of balancing stocks with short-term government bonds highlights the importance of liquidity and risk reduction in any portfolio.

What is the difference between tokenized and traditional munis? Traditional munis involve paper certificates or book-entry records managed by central depositories. Tokenized munis use smart contracts to automate interest payments and principal repayment. This reduces administrative costs and enables 24/7 trading, though it introduces new technological risks that investors must understand.

No comments yet. Be the first to share your thoughts!