What tokenized munis actually are

Tokenized municipal bonds are digital representations of traditional municipal debt. Instead of holding a physical certificate or a paperless entry in a legacy clearinghouse, the bond is issued as a token on a blockchain. The underlying asset remains the same: a loan to a government entity, such as a city or school district, which pays interest and returns principal based on a fixed schedule.

The primary difference lies in how the bond is managed. Traditional municipal bonds rely on intermediaries like the Municipal Securities Rulemaking Board (MSRB) and various clearing houses to track ownership and process payments. This creates administrative friction and can delay settlement. Tokenization replaces much of this manual oversight with smart contracts.

A smart contract is a piece of software stored on the blockchain that automates the execution of the bond’s terms. As the Local Government Commission explains, these agreements can be tokenized to automate the distribution of interest payments and the repayment of principal. This reduces the need for manual reconciliation and can speed up the flow of funds to investors.

For investors, this means the bond still behaves like a standard muni: it offers tax-exempt income and is backed by the creditworthiness of the issuer. However, the digital wrapper allows for faster trading, fractional ownership, and greater transparency in the ledger. It is not a new type of financial instrument, but a new way of recording and transferring an existing one.

The infrastructure behind onchain credit

Tokenizing a municipal bond is not just about moving a PDF onto a ledger; it requires a technical stack that bridges traditional legal obligations with automated on-chain execution. This infrastructure relies on three core components: the blockchain network for settlement, custody solutions for security, and oracle networks to verify off-chain events.

The blockchain acts as the settlement layer. For tokenized municipal bonds, issuers typically choose permissioned or regulated public chains that offer high throughput and compliance-friendly environments. These ledgers record the bond’s lifecycle—from issuance to maturity—ensuring that every transfer is immutable and transparent. The choice of chain often depends on the custodian’s existing relationships and the need for interoperability with traditional financial rails.

Custody is where the digital and physical worlds intersect. Unlike retail crypto wallets, institutional custody for tokenized bonds involves multi-signature schemes and hardware security modules (HSMs) to protect private keys. This layer ensures that the token representing the bond is backed by the actual legal claim. If the bond is held in a traditional trust, the custodian must ensure that the on-chain token accurately reflects the off-chain holdings, creating a 1:1 peg between the digital asset and the legal instrument.

Oracle networks bridge the gap for events that happen outside the blockchain. When a municipality makes a coupon payment or defaults on a bond, that information must be fed into the smart contract to trigger the appropriate action. Oracles verify these off-chain data points and update the on-chain state, ensuring that automated payments and compliance checks execute correctly. Without reliable oracles, the smart contract cannot enforce the bond’s terms autonomously.

Market research and regulatory sandbox

Tokenized US Municipal Bonds works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Strategy for institutional and retail access

Tokenized municipal bonds are reshaping how different investor types interact with fixed income, but the path to entry varies significantly between institutions and retail participants. For institutions, the primary value lies in operational efficiency and balance sheet optimization. By moving from traditional custodial chains to blockchain-based settlement, banks and asset managers can reduce counterparty risk and settle trades in near real-time. This fractionalization allows large portfolios to hold smaller, diversified slices of municipal debt without the administrative overhead of managing thousands of individual certificates.

Retail investors face a different landscape, though the barriers are lowering. Historically, municipal bonds required significant capital minimums and were largely inaccessible to individual traders. Tokenization removes these friction points, allowing investors to buy fractions of bonds with smaller amounts of capital. However, regulatory frameworks remain the gatekeeper. The SEC and MSRB (Municipal Securities Rulemaking Board) are actively evaluating how these digital assets fit into existing securities laws, particularly regarding investor accreditation and secondary market liquidity.

Liquidity and Tax Nuances

The promise of 24/7 liquidity is a major draw, but it comes with caveats. Unlike stocks, municipal bonds often trade in less active markets. While tokenization can increase trading frequency, the underlying liquidity depends on the depth of the secondary market for that specific bond issuance. Investors must also consider the tax implications. The tax-exempt status of municipal bond interest remains a key feature, but tokenization introduces new questions about how "constructive receipt" of income is handled in a digital environment. Always consult a tax professional to understand how holding digital securities affects your specific tax situation.

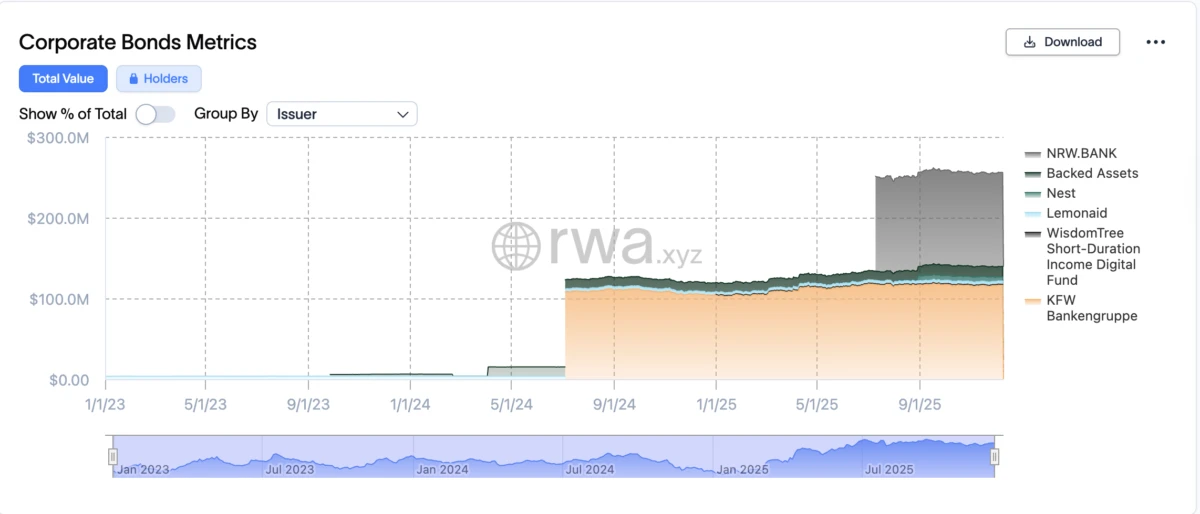

The broader trend of tokenized assets

The market for tokenized real-world assets (RWA) has shifted from experimental pilots to a structural component of modern finance. While the total market capitalization is still a fraction of traditional fixed-income markets, the growth trajectory signals a fundamental change in how debt instruments are issued and traded. This section examines the technical indicators driving this expansion.

The primary driver is not speculation, but utility. Tokenization solves specific friction points in municipal and treasury bond markets: settlement times, minimum investment thresholds, and liquidity fragmentation. By moving these assets onto public or permissioned ledgers, issuers can access a broader base of retail and institutional capital that was previously locked out by operational inefficiencies.

To visualize this momentum, we look at the performance of broader RWA indices. The chart below tracks the market cap of leading tokenized asset protocols, providing context for the specific growth seen in municipal bond tokenization.

This upward trend reflects institutional adoption rather than retail hype. Major financial institutions are increasingly integrating blockchain infrastructure to handle bond issuance, secondary trading, and compliance automation. The technical infrastructure is stabilizing, reducing the counterparty risks that previously hindered widespread adoption.

Checklist for evaluating tokenized bond platforms

Tokenized municipal bonds offer efficiency, but they introduce new technical and regulatory risks that traditional bondholders rarely face. Before committing capital, you need a concrete workflow to assess the platform’s integrity. This checklist breaks down the essential due diligence steps for security, compliance, and liquidity.

Ensure the token represents a direct, legally enforceable claim on the underlying municipal bond. The platform must clearly link the token to the issuer and the specific bond offering, ideally through a registry recognized by the Municipal Securities Rulemaking Board (MSRB). If the legal wrapper is ambiguous, your token may not hold the same rights as the traditional security.

Who holds the private keys, and how are price feeds verified? For municipal bonds, liquidity can be thin, making oracle manipulation a real risk. Look for platforms that use institutional-grade custodians and transparent, audited oracle mechanisms that source data directly from primary market dealers or official MSRB reporting tools.

Tokenized munis are securities, meaning they must adhere to SEC and MSRB regulations. Verify that the platform performs robust Know Your Customer (KYC) and Anti-Money Laundering (AML) checks on every transaction. Compliance isn't just a feature; it's the foundation that prevents the platform from being shut down or the tokens from being frozen.

Unlike Treasury bills, municipal bonds can be illiquid. Check if the platform provides guaranteed liquidity pools or has partnerships with primary dealers who stand ready to buy back tokens. Without a clear exit strategy, you could be stuck holding a token that represents a valid bond but cannot be sold when you need to.

By following this structured approach, you can separate legitimate tokenization efforts from speculative experiments. The goal is to ensure that the digital wrapper adds efficiency without compromising the legal and financial safeguards that make municipal bonds a staple of conservative portfolios.

Can you tokenize bonds effectively?

The short answer is yes, but the execution is still maturing. Tokenizing bonds works for liquid assets like cash and crypto, and increasingly for historically illiquid assets like private credit. The core promise is automation: smart contracts can execute agreements and distribute payments without manual intervention, reducing friction and settlement time.

However, "effectively" depends on your definition. While the technology is viable, the ecosystem is fragmented. You are not just buying a digital asset; you are navigating a new regulatory layer. The Local Government Commission and other official bodies are actively studying how to integrate these digital instruments into existing municipal finance frameworks. Until standards are universal, liquidity remains the primary bottleneck.

For investors, the benefit is clear: fractional ownership and 24/7 settlement. For issuers, the benefit is access to a broader, global pool of capital. But the limitations are real. Interoperability between different blockchain platforms is not yet seamless, and regulatory clarity varies wildly by jurisdiction. You need to look at official sources, like the SEC and MSRB, to understand the compliance landscape before assuming tokenization is a plug-and-play solution.

No comments yet. Be the first to share your thoughts!