Why tokenized muni bonds matter now

The traditional municipal bond market operates like a heavy freight train: reliable, but slow to turn. For decades, issuers have navigated a fragmented ecosystem of intermediaries, manual settlement processes, and high compliance costs. While these bonds remain a cornerstone of American infrastructure financing, the friction in the system creates inefficiencies that blockchain technology is uniquely positioned to resolve.

The core problem is structural. Issuing a municipal bond today involves a lengthy chain of underwriters, trustees, and transfer agents. Each layer adds cost and time, often resulting in higher interest rates for municipalities and limited access for smaller investors. The Local Government Commission (LGC) has noted that tokenized public debt offers a path to expand the bond market, increase inclusion, and significantly reduce issuance costs by streamlining these processes.

Regulatory frameworks are beginning to catch up with this potential. The Securities and Exchange Commission (SEC) has proposed a regulatory sandbox for market modernization, envisioning an environment where municipalities can issue tokenized representations of traditional securities. This structured approach allows for testing new technologies while maintaining investor protections, signaling that the barrier to entry for tokenized instruments is lowering.

This shift isn't just about speed; it's about accessibility. By tokenizing bonds, municipalities can potentially lower interest rates through increased market participation and reduced administrative overhead. The SEC’s focus on a sandbox framework suggests a cautious but deliberate move toward integrating blockchain into the core of public debt issuance, promising a more efficient and inclusive market for both issuers and investors.

Tracking the tokenized muni bond market

Use this section to make the Tokenized US Municipal Bonds Market Research decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

The technical and regulatory infrastructure behind onchain credit

Tokenized municipal bonds are not just digital copies of paper certificates; they require a specialized stack that bridges traditional finance with blockchain technology. This infrastructure must satisfy two masters: the immutable speed of distributed ledgers and the rigid compliance requirements of US securities law. Without this dual-layer approach, tokenized munis cannot exist in a regulated market.

Blockchain selection and settlement

The underlying blockchain acts as the settlement layer. Unlike consumer cryptocurrencies, institutional tokenization typically occurs on permissioned or regulated public chains that offer finality and auditability. The goal is to reduce the settlement cycle from T+2 to near-instant, eliminating counterparty risk. This requires a network that can handle high throughput while maintaining the strict data integrity required by custodians and transfer agents.

Smart contract mechanics

Smart contracts automate the lifecycle of the bond. They handle coupon payments, maturity redemptions, and corporate actions. However, these contracts must be audited rigorously, as they hold real-world value. The code must be immutable once deployed, ensuring that the terms of the bond—interest rates, payment dates, and principal amounts—are executed exactly as written, without human intervention or error.

Compliance layers and KYC/AML

The most critical component is the compliance layer. Municipal bonds are securities, meaning they are subject to strict Know Your Customer (KYC) and Anti-Money Laundering (AML) regulations. Token wallets must be integrated with identity verification systems. If a wallet fails a compliance check, the smart contract can restrict transfers, ensuring that only accredited or qualified investors can hold the token. This "programmable compliance" is what makes tokenized munis legally viable.

The Securities and Exchange Commission (SEC) has outlined frameworks for this integration. Their proposed regulatory sandbox for tokenized municipal instruments envisions a structured environment where these compliance checks are baked into the token’s design from issuance. This ensures that the benefits of blockchain technology do not come at the cost of regulatory oversight.

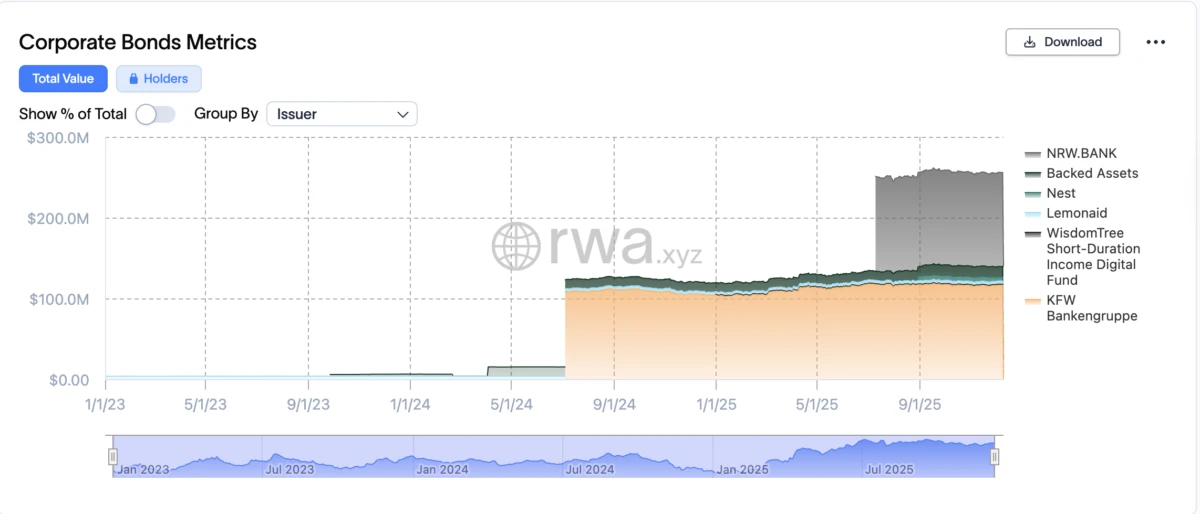

Note: The chart above illustrates the volatility and trading volume of municipal bank holding companies, a sector heavily influenced by municipal bond market health. Tokenized munis aim to bring similar liquidity to the underlying debt instruments.

Accessing the Infrastructure: Platforms and Tools

Tokenized municipal bonds are not traded on open consumer exchanges like stocks. Instead, access requires specialized infrastructure platforms that bridge traditional fixed-income settlement with blockchain rails. These platforms handle the complex regulatory compliance, KYC/AML checks, and custody solutions necessary for high-stakes finance.

Institutional-Grade Platforms

The primary tools for accessing tokenized munis are permissioned platforms operated by major financial institutions and fintech innovators. Firms like J.P. Morgan (Onyx) and Franklin Templeton have built internal networks or partner with blockchain protocols to facilitate these trades. For retail or accredited investors, access is often gated through regulated broker-dealers or tokenization platforms that integrate with existing brokerage accounts.

The infrastructure typically involves a "wrapper" token that represents the underlying bond. This token is minted on a blockchain (often Ethereum or private chains like Quorum/Hyperledger) and settles in near real-time, eliminating the traditional T+1 or T+2 settlement lag. Investors interact with these tools through dashboards that mirror traditional trading interfaces but execute on-chain.

Essential Research and Market Data Tools

To evaluate tokenized munis effectively, investors rely on data aggregators that track both the traditional bond market and the emerging digital asset space. Platforms like Bloomberg Terminal and Refinitiv Eikon provide baseline yield data for traditional munis, which serves as a benchmark for tokenized equivalents. For on-chain specific metrics, tools like Dune Analytics or specialized DeFi dashboards track liquidity and volume on tokenization platforms.

For those looking to deepen their understanding of the underlying technology, the following resources provide a solid foundation in blockchain infrastructure and tokenized assets.

As an Amazon Associate, we may earn from qualifying purchases.

Key Considerations for Platform Selection

When choosing a platform to access tokenized munis, verify that the provider is registered with the SEC and complies with MSRB rules. The platform should offer transparent custody solutions, ensuring that the underlying bond is held in a segregated account. Additionally, check for integration with traditional banking rails to facilitate easy fiat on-ramps and off-ramps.

Can you tokenize bonds?

The short answer is yes. The SEC has confirmed that tokenized securities are legally recognized as securities, meaning existing frameworks for stocks, bonds, and notes apply directly to their digital counterparts.

The SEC’s recent proposal for a regulatory sandbox framework envisions a structured environment where participating municipalities can issue tokenized representations of traditional instruments. This approach aims to test modernization while maintaining investor protection standards.

No comments yet. Be the first to share your thoughts!