What tokenized muni bonds actually are

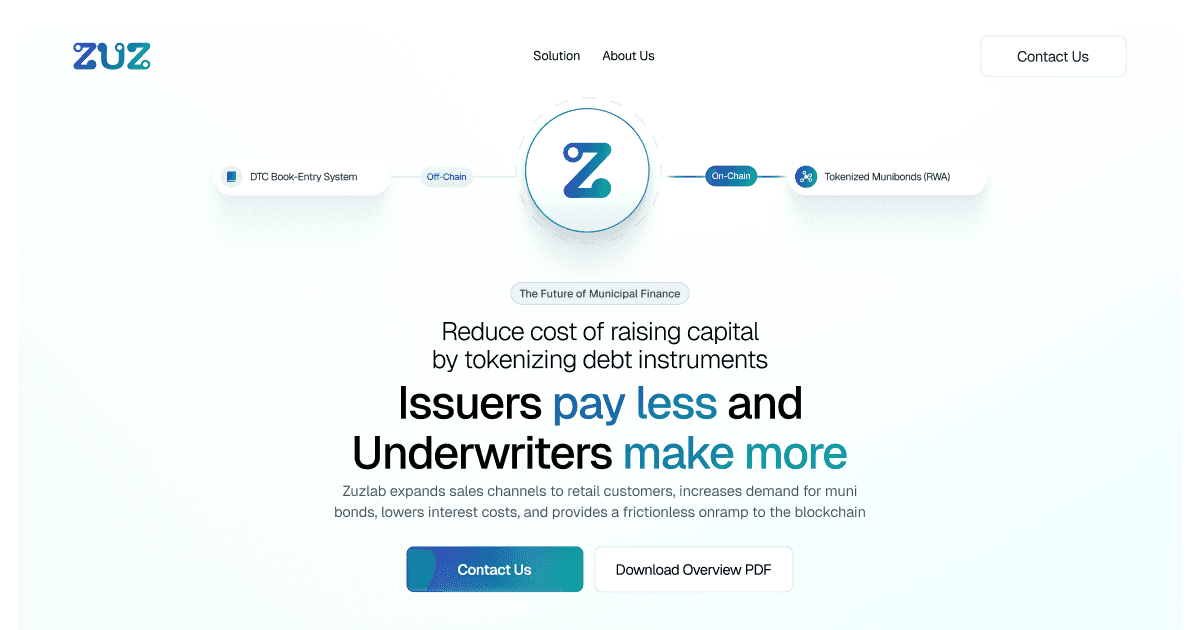

Tokenized municipal bonds represent a structural upgrade to how debt is settled, rather than a change in the underlying asset. When you buy a traditional municipal bond, you are lending money to a government issuer in exchange for a promise of regular interest payments and the return of face value at maturity MSRB. The ownership of that debt is recorded by a central depository, such as DTC, and transfers between investors happen through a chain of brokers, custodians, and clearinghouses. This process, known as T+2 settlement, introduces delays and intermediaries that can slow capital flow.

Tokenization encodes the same ownership, transfer rights, and economic terms into a digital token on a blockchain. The underlying debt obligation remains identical: the issuer still owes the same principal and interest. However, the ledger changes. Instead of relying on a centralized, siloed database, the bond’s lifecycle is recorded on a distributed ledger. This shift transforms the settlement layer, allowing for faster, more transparent, and potentially automated execution of trades and payments.

This distinction matters because it separates the risk of the issuer from the risk of the settlement infrastructure. In a tokenized muni bond, the primary credit risk remains with the municipal entity issuing the debt. The technology layer introduces new operational considerations, such as custody and smart contract security, but it does not alter the fundamental nature of the loan. By moving the record-keeping to a blockchain, the market aims to reduce friction, lower costs, and increase liquidity for an asset class that has historically been illiquid and fragmented.

Market infrastructure and settlement layers

Tokenized municipal bonds rely on a hybrid plumbing system that merges traditional financial custody with blockchain settlement. The process begins with a digital representation of the bond, structured as a security compliant with existing securities laws. This digital twin is not a standalone asset; it is a cryptographic claim on the underlying municipal debt, governed by legal agreements that define investor rights, coupon payments, and maturity dates.

Smart contracts and automation

At the core of this infrastructure are smart contracts. These are pieces of software stored on a blockchain that automate the execution of bond terms. Instead of relying on manual processing for interest payments or principal redemption, the smart contract executes these actions automatically when predefined conditions are met. This reduces administrative friction and minimizes the risk of human error in settlement.

Custody and regulatory oversight

Secure custody is critical for tokenized assets. Tokens must be held in robust storage solutions to prevent loss or theft, a challenge that requires specialized custodial services. Regulatory bodies are adapting to this new infrastructure. The SEC has proposed sandbox frameworks to test tokenized securities, allowing for controlled experimentation with digital representations of traditional municipal debt. These pilots help clarify how existing securities laws apply to blockchain-based instruments.

Market context

Understanding the broader market volatility is essential when evaluating tokenized municipal bonds. The performance of traditional muni ETFs often serves as a benchmark for the underlying asset class.

Yield advantages and tax implications

Tokenized municipal bonds offer a compelling economic case by preserving the tax-exempt status of traditional munis while unlocking fractional ownership. This structure allows investors to access high-quality debt with lower capital requirements, effectively democratizing access to steady, tax-advantaged income streams.

The primary advantage lies in the yield pickup relative to risk-adjusted returns. By reducing the minimum investment threshold, tokenization enables broader participation in the municipal bond market. Investors can build diversified portfolios across multiple issuers and sectors, mitigating concentration risk that is often prohibitive in traditional secondary markets. This fractional approach maintains the favorable federal—and often state—tax treatment that makes munis a strategic exposure for income-focused clients.

However, the tax efficiency of tokenized assets requires careful navigation. While the underlying bond retains its tax-exempt character, the act of trading tokens can introduce reporting complexities. Selling or trading tokenized assets may create significant tax reporting challenges, particularly regarding cost basis tracking across blockchain transactions. Additionally, custodial risks associated with secure storage and management of digital tokens must be managed through robust solutions to prevent loss or mismanagement.

To understand the structural differences between holding traditional munis versus tokenized versions, consider the following comparison of liquidity, entry barriers, and settlement mechanics.

| Feature | Traditional Muni Bonds | Tokenized Muni Bonds |

|---|---|---|

| Minimum Investment | $5,000–$10,000+ | $100–$500 |

| Liquidity | Low (OTC market, days to settle) | High (24/7 trading, minutes to settle) |

| Tax Reporting | Standard 1099-INT | Complex (potentially requiring crypto tax software) |

| Custody | Brokerage/DTC | Digital Wallet/Smart Contract |

Regulatory sandbox and compliance status

Tokenized US municipal bonds operate within a carefully monitored regulatory environment. The Securities and Exchange Commission (SEC) has established a regulatory sandbox framework specifically designed to test market modernization. This pilot program allows eligible participants to issue tokenized securities that serve as digital representations of traditional municipal debt instruments. By testing these instruments in a controlled setting, regulators can assess operational risks and investor protection mechanisms before broader adoption.

The Municipal Securities Rulemaking Board (MSRB) provides the foundational rules for secondary market trading and reporting. While the MSRB primarily oversees traditional bond transactions, its guidelines on transparency, anti-fraud measures, and fair dealing form the baseline for compliance. Any entity participating in tokenized muni markets must align with these established norms to ensure legal safety and market integrity.

Investors should verify that tokenized offerings are conducted through registered broker-dealers or exempt marketplaces that adhere to SEC oversight. The sandbox approach signals a cautious but open stance from regulators, prioritizing stability over rapid innovation. As the framework evolves, participants gain clarity on custody requirements, tax reporting obligations, and cross-border interoperability standards.

Downsides and Custody Risks

Tokenized US municipal bonds promise efficiency, but they introduce distinct technical and operational risks that traditional bondholders rarely face. The shift from paper or central ledger records to blockchain-based assets requires investors to manage new vulnerabilities in smart contracts and custody solutions.

Smart Contract Vulnerabilities

Tokenization relies on smart contracts—self-executing code that automates coupon payments and maturity distributions. While these agreements reduce administrative overhead, they also create a single point of failure. If the code contains a bug or is exploited, the automated execution of bond terms can be compromised, potentially leading to financial loss or frozen assets.

Custodial Complexity

Holding tokenized assets requires robust digital storage solutions that differ significantly from traditional brokerage accounts. Tokens can be lost if private keys are misplaced or stolen if security protocols are breached. Unlike a registered bond held by a central depository, the responsibility for securing the asset often shifts more directly to the investor or their chosen custodian.

Tax Reporting Challenges

Selling or trading tokenized assets can create significant tax reporting challenges. The immutable nature of blockchain transactions means every trade is recorded, but these records may not automatically align with traditional tax reporting formats. Investors must often manually track cost basis and capital gains for each tokenized transaction, increasing the administrative burden compared to traditional bond trading.

No comments yet. Be the first to share your thoughts!