What are tokenized municipal bonds?

Tokenized municipal bonds are digital representations of traditional debt securities recorded on a blockchain. A muni bond is a loan made to a city, county, or state government to fund public projects like schools, roads, or water systems. When tokenized, ownership rights and payment flows are tracked on a distributed ledger rather than in a central depository.

The token acts as a digital certificate of ownership. It does not change the underlying asset—the government still owes the same interest and principal—but it changes how that ownership is tracked and transferred. Instead of paper certificates or electronic entries in a legacy system, the bond exists as a cryptographic token. This distinction matters because the token is not a new financial instrument; it is a wrapper around an existing legal claim. The value comes from the underlying municipal issuer, not the blockchain technology.

By separating the legal obligation from the settlement layer, tokenization aims to make municipal bonds more accessible and liquid. However, the fundamental risk remains the same: you are lending money to a government entity. If that entity struggles to pay its bills, the token's value drops just as it would for a traditional bond.

The infrastructure behind tokenization

Tokenized municipal bonds are not magic; they are a stack of software and legal agreements working together. Behind every digital bond on a ledger is a traditional legal structure that defines ownership, interest payments, and default remedies. The technology simply moves this structure from paper and central clearinghouses to a distributed network.

Custody and legal wrappers

Before a bond becomes a token, it must exist in a legal form that a blockchain can represent. This usually involves a "legal wrapper"—a smart contract that mirrors the rights of the traditional bondholder. When you hold the token, you hold a digital claim on the underlying municipal debt.

Custody is the next layer. Just as you wouldn't leave physical bond certificates in an unsecured envelope, tokenized assets require secure digital custody. Institutions use multi-signature wallets or specialized custodial services to manage the private keys that control these tokens. This ensures that only authorized parties can transfer ownership or access interest payments.

Smart contracts and distributed ledgers

Smart contracts automate the tedious parts of bond management. They handle coupon payments, maturity redemptions, and compliance checks without human intervention. If a bond pays interest quarterly, the smart contract sends the funds to all token holders automatically when the date arrives. This reduces administrative costs and settlement risk.

These contracts run on distributed ledgers, which serve as the public record of ownership. Unlike a central database, the ledger is shared among all participants. This transparency helps regulators and auditors verify transactions in real time. It also means that trades can settle almost instantly, rather than waiting days for traditional clearing processes.

Trading and settlement

The combination of smart contracts and ledgers changes how bonds are traded. In traditional markets, buying a municipal bond involves brokers, dealers, and clearinghouses, often taking T+1 or T+2 days to settle. On a blockchain, the trade and the settlement happen simultaneously. This "atomic settlement" eliminates the risk that one party defaults before the other delivers the asset.

This efficiency is particularly valuable for institutional investors who manage large portfolios of municipal debt. They can rebalance holdings faster and with lower transaction costs. However, the technology is still evolving. Regulatory bodies like the SEC and MSRB are closely watching these developments to ensure investor protection remains intact as the infrastructure matures.

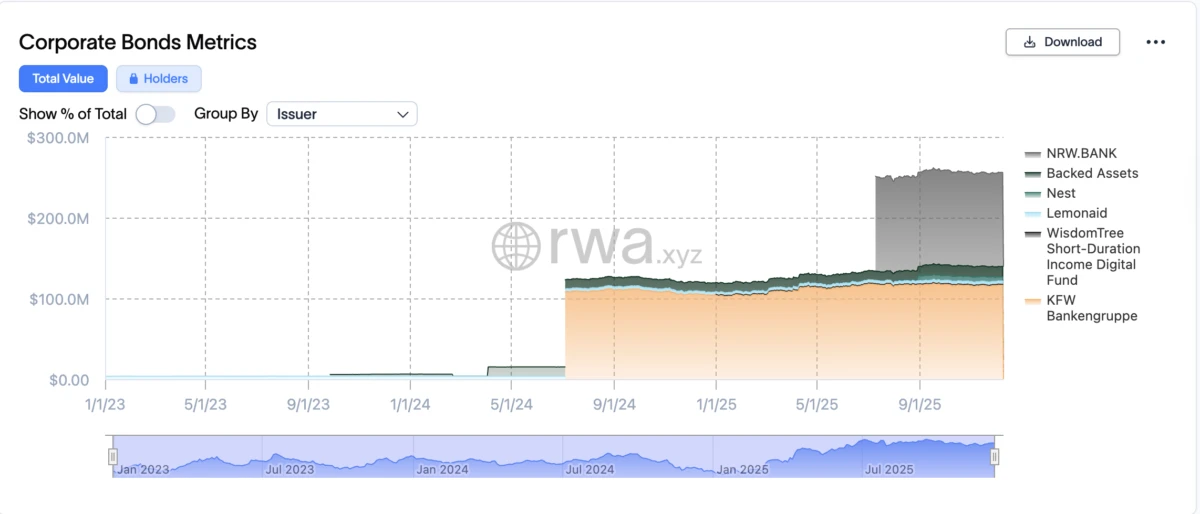

Current State of Tokenized Municipal Bonds

Tokenized municipal bonds are still a niche segment of the broader fixed-income market. While traditional munis trade billions in daily volume on established exchanges, tokenized versions operate on smaller, newer platforms with significantly lower liquidity. This difference matters because it affects how quickly you can enter or exit a position without moving the price.

The infrastructure is maturing, but the ecosystem remains fragmented. Unlike traditional bonds that settle through the Depository Trust Company (DTC), tokenized bonds rely on distributed ledger technology. This creates new operational considerations, such as interoperability between different blockchains and the legal enforceability of smart contract terms. The Securities and Exchange Commission (SEC) has launched a regulatory sandbox to test these frameworks, aiming to clarify how tokenized instruments should be treated under existing securities laws SEC Sandbox Framework.

For now, most tokenized muni activity is driven by institutional players and high-net-worth individuals seeking specific tax advantages or cross-border access. Retail adoption is growing but remains cautious due to the complexity of custody and settlement. If you are considering this asset class, treat it as an emerging infrastructure play rather than a mainstream liquid alternative.

To understand where the market stands, it helps to compare the mechanics of traditional muni ETFs against these new tokenized platforms. The following table highlights the key operational differences that impact investor experience.

| Feature | Traditional Muni ETFs | Tokenized Muni Platforms |

|---|---|---|

| Liquidity | High (Exchange-traded) | Low to Moderate (Platform-dependent) |

| Minimum Investment | Share price (often <$100) | Fractional shares (often <$10) |

| Settlement Time | T+1 or T+2 | Near-instant (Blockchain-dependent) |

| Regulatory Oversight | SEC, MSRB | Evolving (SEC Sandbox, etc.) |

Risks and regulatory considerations

Tokenized US municipal bonds sit at the intersection of two highly regulated worlds: traditional securities law and emerging blockchain infrastructure. While the promise of instant settlement is compelling, the reality involves navigating a complex web of legal structures and technical vulnerabilities. Investors must understand that digitizing a bond does not eliminate the underlying risks; it simply shifts some of them from the back office to the code.

Regulatory uncertainty

The legal framework for tokenized assets is still evolving. Unlike traditional bonds, which are governed by well-established precedents, tokenized securities often exist in a gray area where it is unclear how existing laws apply to digital ledgers. The Securities and Exchange Commission (SEC) has emphasized that tokenization does not change the fundamental nature of the security. If an asset is a security in paper form, it remains a security in digital form.

This means that compliance with securities laws—such as registration requirements and investor accreditation rules—still applies. The SEC’s recent sandbox initiatives aim to clarify these boundaries, but until regulations are fully codified, there is a risk that legal interpretations could shift. Investors should verify the specific legal structure of any tokenized offering to ensure it complies with current securities regulations.

Smart contract risk

The code that manages tokenized bonds is only as secure as its developers. Smart contracts are immutable once deployed, meaning that any bug or vulnerability can lead to irreversible loss of funds. Unlike traditional banking errors, which can often be reversed, a successful hack on a blockchain protocol is final.

Even with rigorous audits, smart contracts remain exposed to novel attack vectors. Investors must assess the security track record of the platform issuing the tokens. This includes reviewing audit reports, understanding the upgradeability mechanisms of the contracts, and evaluating the decentralization of the underlying network. The convenience of digital ownership comes with the responsibility of trusting the technology stack.

Liquidity limits to account for

While tokenization aims to improve liquidity, the reality is often more nuanced. The market for tokenized municipal bonds is still nascent, with limited secondary trading activity. Unlike the deep, liquid market for traditional Treasuries, tokenized munis may face wide bid-ask spreads or difficulty finding buyers during market stress.

Interoperability remains a challenge. If tokens are issued on different blockchains, exchanging them can be complex and costly. The SEC has noted that cross-asset exchanges involving tokenized instruments on different ledgers present significant operational hurdles. Until standardization improves, liquidity may be fragmented, making it harder to exit positions quickly or at fair market value.

How to evaluate tokenized muni opportunities

Tokenized municipal bonds merge traditional credit risk with new technological variables. Before allocating capital, you need a due diligence framework that treats the digital layer with the same scrutiny as the underlying issuer.

Start with the traditional metrics. Check the bond’s credit rating from agencies like Moody’s or S&P. Review the issuer’s financial health, debt-to-revenue ratios, and economic diversification. Tokenization does not change the fundamental obligation of the municipality to pay back principal and interest. If the underlying credit is weak, the digital wrapper offers no protection.

Who is issuing the token? Investigate the fintech company or platform facilitating the tokenization. Look for their track record in digital asset custody, regulatory compliance history, and partnerships with established financial institutions. A reputable issuer reduces counterparty risk and ensures that the digital representation of the bond is backed by clear legal structures.

Security is paramount. Determine how the underlying bond certificates are held. Are they stored in a regulated custodian? How does the platform handle private key management? Look for proof of insurance, regular security audits, and transparent protocols for redemptions. The platform must be robust enough to prevent theft, loss, or unauthorized transfers of your investment.

This checklist ensures you are not just buying a digital token, but a secure claim on a real-world asset. Always prioritize infrastructure stability and regulatory clarity over speculative hype.

No comments yet. Be the first to share your thoughts!