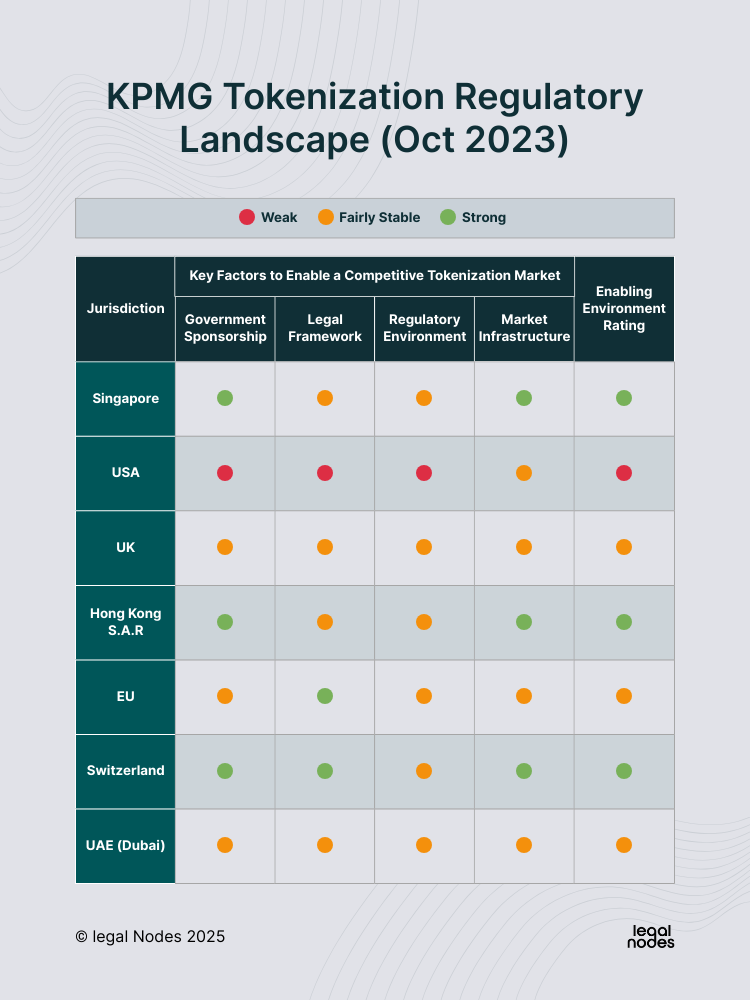

Understand the regulatory sandbox status

Before attempting to access tokenized US municipal bonds, you need to understand where these assets currently sit in the financial ecosystem. They are not yet fully open to the general public. Instead, they are operating within a limited experimental framework known as a regulatory sandbox.

The Securities and Exchange Commission (SEC) has established pilot programs to test the viability of tokenized securities. As outlined in their recent framework documents, tokenized municipal instruments in these pilots are structured as digital representations of traditional municipal debt. This means the underlying asset is still a standard muni bond, but the ownership record is maintained on a blockchain.

This experimental status has two immediate implications for accessibility. First, participation is often restricted to qualified institutional investors or accredited individuals who meet specific criteria set by the pilot sponsors. Second, the liquidity and trading mechanisms are still being refined, so you may not be able to buy or sell these tokens on open, public exchanges in the same way you trade stocks.

Think of the sandbox as a controlled testing ground. The SEC and participating issuers are using it to verify that the technology works securely and complies with existing securities laws. Until the pilot concludes and regulations are fully adapted, access remains narrow. You should treat these tokens as emerging assets with restricted availability rather than mainstream investment vehicles.

For the most accurate details on who can participate in current pilots, refer to the SEC's official framework for tokenized municipal instruments. This document provides the definitive rules governing these experimental programs.

Select a compliant onchain issuer

Choosing the right platform for tokenized US municipal bonds starts with verifying regulatory compliance. Because municipal debt is heavily regulated, legitimate issuers do not operate in the shadows. They maintain clear legal structures that bridge traditional securities law with blockchain technology. Your first step is to identify platforms that offer official backing and transparent smart contracts.

Tokenized bonds are digital representations of traditional bond instruments on a blockchain or distributed ledger. In essence, the token serves as a proof of ownership, automating payments and interest distributions through code. However, the technology is only as safe as the legal framework surrounding it. You need an issuer that has navigated the complex intersection of state and federal securities regulations.

When evaluating potential issuers, look for those that have partnered with established financial institutions or government entities. These partnerships often signal a higher level of due diligence and regulatory scrutiny. Avoid platforms that promise high yields without disclosing their legal structure or custodial arrangements. The goal is to find a bridge between the efficiency of blockchain and the security of traditional finance.

The table below compares key features of prominent tokenized muni issuers, focusing on regulatory status, minimum investment, and yield structure. Use this data to filter out non-compliant options and narrow your search to legitimate platforms.

| Issuer | Regulatory Status | Min. Investment | Yield Structure |

|---|---|---|---|

| Securitize | SEC-registered | $100 | Fixed semi-annual |

| tZERO | SEC-registered | $5,000 | Fixed monthly |

| Propy | State-compliant pilot | $1,000 | Variable |

| Munihub | P2P compliant | $50 | Fixed quarterly |

Set up your digital wallet and identity

Accessing tokenized US municipal bonds requires a bridge between traditional finance compliance and blockchain infrastructure. You cannot simply buy these assets with a standard, non-custodial wallet. The process demands a compatible digital wallet that supports the specific blockchain network of the token and a verified identity that meets strict KYC/AML standards.

1. Choose a compliant digital wallet

Not all wallets can hold or transfer tokenized securities. You need a wallet that supports the specific token standard (often ERC-3643 or similar compliant standards) used by the platform issuing the bonds. Look for wallets that allow you to connect to verified DeFi or security token platforms. Examples include wallets from providers like Ledger or Trezor, provided they integrate with the specific platform’s interface, or web-based wallets offered directly by the tokenization platform.

2. Complete KYC and AML verification

Tokenized municipal bonds are regulated securities. Before you can purchase or hold them, you must undergo Know Your Customer (KYC) and Anti-Money Laundering (AML) checks. This typically involves uploading a government-issued ID, proof of address, and sometimes a selfie for biometric verification. This step is non-negotiable and is required by the platform to ensure you are an accredited or qualified investor, depending on the bond’s structure.

3. Fund your wallet

Once your identity is verified and your wallet is set up, you need to fund it with the cryptocurrency or stablecoin required by the platform. Most tokenized bond platforms operate on Ethereum or other EVM-compatible chains, so you will likely need ETH or USDC. Transfer these funds from a reputable exchange to your wallet address. Double-check the network (e.g., Ethereum Mainnet, Polygon) to avoid sending funds to the wrong chain.

4. Connect to the tokenization platform

Navigate to the platform offering the tokenized municipal bonds. Use the "Connect Wallet" feature to link your digital wallet to their interface. Ensure you are on the official website to avoid phishing sites. The platform will display your wallet balance and any tokens you already hold. If your wallet is not recognized or lacks the necessary permissions, the platform will guide you through any additional setup steps.

5. Select the bond and confirm purchase

Browse the available tokenized US municipal bonds. Review the details, including the yield, maturity date, and issuer. Once you select a bond, the platform will show you the minimum investment amount and the transaction fee. Confirm the transaction in your wallet. The smart contract will then transfer the tokens to your wallet address, and the funds to the issuer. You will receive a transaction hash to verify the transfer on the blockchain.

Execute the purchase and manage yield

Buying tokenized US municipal bonds is a two-step process: acquiring the token and verifying the smart contract. Unlike traditional bonds, you don’t wait for a settlement period; ownership transfers on-chain immediately. However, the mechanics of how interest (yield) flows to your wallet differ significantly from legacy systems.

1. Verify the smart contract and tax status

Before funding the transaction, confirm the token’s contract address matches the official issuer’s registry. A wrong address means lost funds. More importantly, ensure the token is issued in "registered form." According to Alvarez & Marsal, bearer tokens can trigger a 1% excise tax and disqualify the interest from being tax-exempt, destroying the bond’s primary value proposition.

-

Confirm the token contract address matches the official issuer’s registry.

-

Verify the token is issued in "registered form" to preserve tax-exempt status.

-

Check your wallet’s gas fees to ensure you have enough native currency for the transaction.

2. Execute the on-chain transaction

Connect your wallet to the authorized platform and execute the purchase. This is a standard ERC-20 or similar token transfer. The smart contract mints the bond tokens to your address and deducts the principal from your stablecoin or crypto balance. Unlike traditional markets, this happens instantly, 24/7, without waiting for T+1 or T+2 settlement.

3. Manage yield distribution

Interest on tokenized munis is typically distributed via automated smart contract payments rather than manual coupon checks. These payments usually occur quarterly and are sent directly to your wallet address. Because the blockchain records every transaction, you have a transparent, immutable history of all yield distributions. This automation reduces administrative overhead but requires you to monitor your wallet for incoming transfers.

4. Track tax implications

While the bond interest is often federally tax-exempt, state tax treatment varies based on your residency and the issuer’s location. Also, if you trade the token on a secondary market, capital gains tax may apply. Keep detailed records of your on-chain transactions, as these serve as your primary tax documentation. Consult a tax professional to understand how your specific jurisdiction treats digital asset income.

Check common mistakes and fixes

Tokenized municipal bonds offer access, but they come with structural risks that traditional bondholders rarely face. The primary pitfall is liquidity. Unlike on-chain tokens that trade continuously, many tokenized bond platforms operate on private secondary markets or have limited buyer pools. You might find a token listed, but no one to buy it from you when you need to exit. This isn't a bug; it's a feature of private credit. If you need immediate access to cash, tokenized bonds are not the right vehicle.

Smart contract risk is the second major hurdle. When you hold a tokenized bond, you are not just holding a claim on a municipality; you are holding a claim on code. If the smart contract has a vulnerability, your investment could be compromised. Always verify the audit status of the platform. Look for audits from reputable firms like OpenZeppelin or Trail of Bits. Never assume that just because a bond is "tokenized," the underlying legal structure is immune to technical failure.

Tax misclassification is the final trap. The IRS treats tokenized securities based on their economic substance, not their digital form. If the token is structured as a security, standard capital gains and interest rules apply. However, if the platform miscalculates the withholding or reporting, you could face unexpected tax liabilities. Ensure the platform provides clear tax documentation, such as Form 1099-INT or 1099-B, and consult a tax professional familiar with digital assets before investing.

Frequently asked questions about tokenized munis

Work through 2026 Guide: How to Access Tokenized US Municipal Bonds Using Onchain Infrastructure and Yield Strategies

No comments yet. Be the first to share your thoughts!