What are tokenized municipal bonds?

Tokenized municipal bonds are digital representations of traditional debt instruments on a blockchain or distributed ledger. In essence, they take the familiar structure of a municipal bond—issued by states, cities, or counties to fund public projects—and convert ownership into a digital token.

According to the SEC’s Investor.gov, municipal bonds are debt securities issued by governmental entities to fund day-to-day obligations and infrastructure projects. Tokenization does not change the underlying asset or its legal claims; it changes how ownership is recorded and transferred. Instead of holding paper certificates or relying on traditional clearinghouses, investors hold tokens that represent their share of the bond’s principal and interest payments.

This process is often managed through a smart contract, which is a piece of software stored on a blockchain that automates the execution of agreements. As noted by the Pennsylvania Local Government Commission, these contracts can automate interest payments and settlement, reducing the need for manual processing and intermediaries. The result is a more efficient way to access a market traditionally reserved for institutional investors or high-net-worth individuals.

Note: Tokenized bonds are digital tokens on a blockchain that represent ownership in a traditional municipal bond, automating interest payments and settlement via smart contracts.

For onchain investors, this means gaining exposure to the tax-advantaged income stream of munis with the liquidity and transparency of blockchain technology. It is a bridge between the stability of traditional public finance and the innovation of decentralized finance.

The infrastructure behind onchain credit

Tokenized municipal bonds are not just digital replicas of paper certificates; they are engineered financial instruments that rely on a specific blend of regulatory oversight and automated code. For onchain investors, understanding this dual-layer infrastructure is essential to assessing risk and liquidity.

Regulatory frameworks and the SEC sandbox

The viability of these assets rests on evolving regulatory structures. The U.S. Securities and Exchange Commission (SEC) has introduced a regulatory sandbox framework designed to test market modernization. This pilot program allows tokenized securities to operate as digital representations of traditional municipal debt instruments within a controlled environment.

By participating in this sandbox, issuers and platforms can navigate compliance requirements while demonstrating that tokenization can maintain the integrity of traditional municipal markets. The SEC’s approach emphasizes investor protection and market stability, ensuring that the transition from offchain to onchain does not compromise the legal standing of the underlying debt.

Smart contract automation

Beyond regulation, the operational backbone of tokenized bonds is the smart contract. These are self-executing pieces of software stored on a blockchain that automate the execution of agreements. In the context of municipal bonds, smart contracts handle critical functions such as interest payments, principal redemption, and compliance checks.

This automation reduces administrative friction and minimizes the risk of human error. When a bond reaches maturity or a coupon payment is due, the smart contract executes the transfer of funds automatically, ensuring timely and accurate settlement. This layer of code works in tandem with regulatory oversight to create a transparent and efficient investment vehicle.

Why go onchain for municipal bonds?

Tokenized municipal bonds offer structural advantages that address the traditional friction points of the fixed-income market. While the underlying asset remains the same debt obligation issued by a state or local government, the settlement and liquidity mechanics change significantly when moved on-chain. This shift matters for investors who need faster access to capital or want to reduce the operational drag of traditional clearing houses.

Settlement speed and finality

Traditional municipal bond trades often settle on a T+1 or T+2 basis, depending on the market and the specific security. This delay ties up capital and introduces counterparty risk during the settlement window. Tokenized bonds can settle near-instantly or within minutes, depending on the blockchain infrastructure. This speed allows for more efficient capital deployment and reduces the time money is idle between trade execution and ownership transfer.

Liquidity and fractional ownership

The secondary market for municipal bonds is historically fragmented and less liquid than equities or government treasuries. Tokenization can unlock liquidity by enabling fractional ownership. Instead of buying a whole bond with a $5,000 or $100,000 minimum, investors can purchase smaller fractions. This lowers the barrier to entry and creates a deeper pool of potential buyers, which can narrow bid-ask spreads over time.

Comparison: Traditional vs. Tokenized Munis

The following table highlights the structural differences between holding municipal bonds through traditional channels versus on-chain platforms.

| Feature | Traditional Muni Bonds | Tokenized Muni Bonds |

|---|---|---|

| Settlement Time | T+1 to T+2 days | Minutes to hours |

| Minimum Investment | $5,000 - $100,000 | Fractional (e.g., $100+) |

| Secondary Market Liquidity | Fragmented, dealer-driven | Potentially deeper, 24/7 access |

| Custody & Transfer | Physical or DTC book-entry | Digital wallet ownership |

| Dividend/Interest Payments | Semi-annual, via trustee | Automated smart contract distribution |

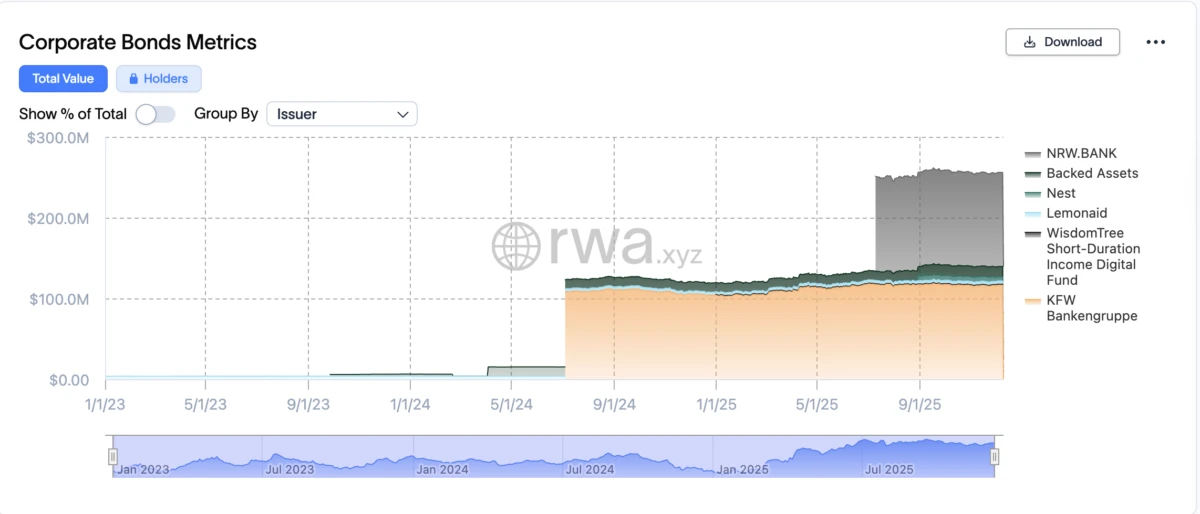

Market research and risk factors

Tokenized US municipal bonds promise efficiency, but they carry the same structural risks as traditional munis, amplified by onchain complexity. Before committing capital, you need to understand where the money actually goes and what happens when things go wrong.

Credit risk is real

Municipal bonds are debt obligations. If a city or county defaults, token holders are unsecured creditors with no government backstop. The 2013 Detroit bankruptcy showed that even large municipalities can struggle. Today, many local governments face structural deficits from pension liabilities and infrastructure decay. Tokenization doesn’t change the underlying cash flow. You’re still exposed to the issuer’s ability to pay.

Regulatory uncertainty

The SEC and MSRB have not fully clarified how tokenized securities fit into existing frameworks. While Regulation D and Reg S offer pathways, compliance varies by jurisdiction. Smart contracts may not hold up in court if they conflict with state law. This legal gray area adds friction to secondary trading and recovery in distress.

Liquidity is not guaranteed

Onchain liquidity can vanish quickly. During market stress, bid-ask spreads widen, and order books dry up. Unlike traditional bonds with dealer support, tokenized munis rely on automated market makers or thin order books. You may not be able to exit your position at a fair price.

The iShares National Muni Bond ETF (MUB) provides a benchmark for muni market health. Watch its price action for signs of stress. If MUB drops sharply, tokenized munis will likely follow, often with greater volatility due to lower liquidity.

Checklist for evaluating tokenized bonds

Before allocating capital to onchain credit, you must verify both the traditional legal structure and the digital infrastructure. Tokenized municipal bonds are digital representations of traditional debt instruments, but they introduce new technical risks that standard due diligence doesn't cover. This checklist ensures you aren't just buying a token, but a fully enforceable claim on municipal debt.

Check if the issuer is registered with the Securities and Exchange Commission (SEC) and if the offering complies with Municipal Securities Rulemaking Board (MSRB) guidelines. The SEC’s recent sandbox frameworks highlight that tokenized securities must maintain the same regulatory protections as their traditional counterparts. Look for explicit filings that confirm the token is a direct digital representation of the underlying bond.

Demand independent security audits from reputable firms for the token’s smart contract. Unlike traditional bonds, code vulnerabilities can lead to irreversible loss of principal. Ensure the audit covers minting, burning, and transfer functions, and verify that the contract owner has limited privileges to prevent unauthorized changes to the token supply or distribution logic.

Identify the legal entity holding the underlying municipal bonds. The token should be backed by a trusted custodian that holds the actual debt instruments in a segregated account. Verify that the legal wrapper clearly defines your rights as a token holder, including entitlement to interest payments and principal repayment upon maturity.

Understand how and when you can exit the position. Unlike traditional bonds traded on secondary markets, tokenized bonds may have specific redemption windows or limited liquidity pools. Check if there is a buyback program or a designated marketplace for secondary trading, and calculate the potential slippage costs for large exits.

Confirm how interest payments are distributed. Many tokenized bonds use oracles to fetch off-chain payment data and trigger on-chain transfers. Verify the reliability of these oracles and the stability of the stablecoin or fiat gateway used for payouts. A failure in this chain can delay or prevent interest payments, even if the issuer is solvent.

No comments yet. Be the first to share your thoughts!