What tokenized municipal bonds actually are

Tokenized municipal bonds are digital representations of traditional debt instruments. When you buy a standard municipal bond, you are lending money to a local government or agency in exchange for a promise of regular interest payments and the return of face value at maturity MSRB. The ownership is recorded in a central depository, and transfers happen through slow, paper-heavy settlement processes managed by custodians.

Tokenization replaces that paper infrastructure with smart contracts on a distributed ledger. A smart contract is software that automates the execution of agreements, recording ownership and interest payments directly on-chain Local Government Commission. This shift doesn't change the underlying debt obligation—the issuer still owes the money—but it changes how that ownership is tracked, transferred, and settled.

The value proposition lies in efficiency. Traditional bond markets often rely on T+2 or longer settlement cycles, involving multiple intermediaries like clearinghouses and custodians. Tokenized versions can settle in minutes or seconds, reducing counterparty risk and freeing up capital that would otherwise be tied up in settlement processes. For investors, this means faster access to liquidity and potentially lower transaction costs.

It is possible to tokenize any type of security, including bonds and notes SEC. The legal structure remains intact, but the operational layer becomes digital-native. This allows for features like automated interest payments, fractional ownership, and real-time transparency into bond covenants, which were previously difficult to monitor in traditional markets.

Why tokenized munis matter

To understand the appeal of tokenized municipal bonds, you first need to look at the underlying asset. Municipal bonds, or "munis," are debt securities issued by states, cities, counties, and other local governmental entities to fund day-to-day obligations and large-scale projects. As the U.S. Securities and Exchange Commission notes, these instruments are fundamentally securities, meaning the same legal and financial principles apply whether they are held in a traditional book-entry system or represented as digital tokens on a blockchain.

The primary driver for investing in munis has always been their tax advantage. Interest earned on most municipal bonds is exempt from federal income tax, and if you reside in the issuing state, it is often exempt from state and local taxes as well. This tax-exempt status makes munis particularly attractive for investors in higher tax brackets. When these bonds are tokenized, the underlying cash flows and tax attributes remain unchanged; the token simply serves as a more efficient, programmable wrapper for the debt.

Beyond tax benefits, munis represent a critical funding source for public infrastructure. The revenue generated from these bonds pays for schools, highways, water systems, and hospitals. By moving this asset class on-chain, issuers and investors gain access to 24/7 settlement, fractional ownership, and improved liquidity. This efficiency does not alter the fundamental credit risk of the issuer but can lower the cost of capital for municipalities and expand the investor base.

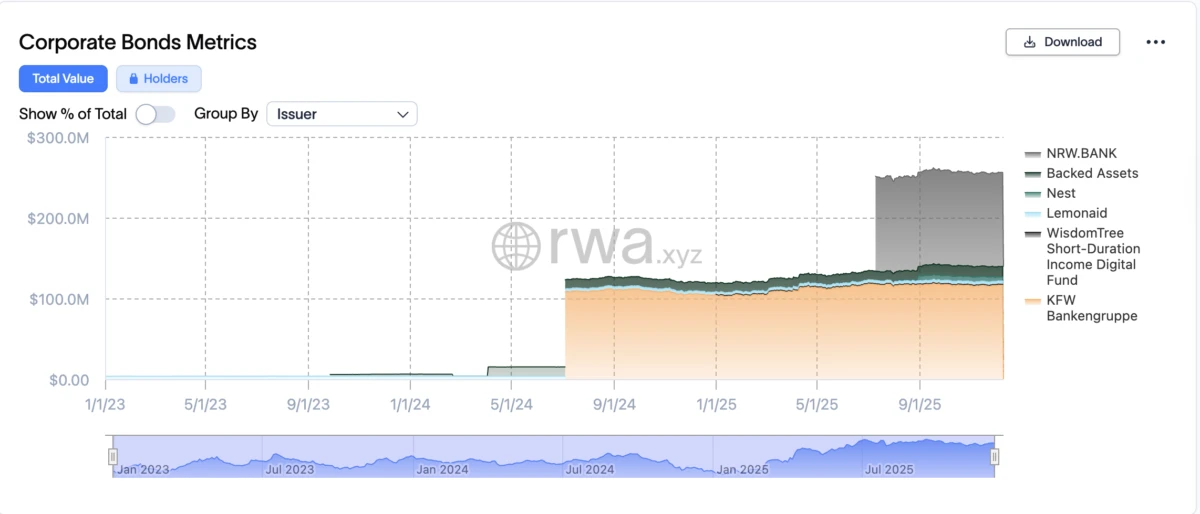

To contextualize the traditional market these tokens are entering, consider the performance of broad municipal bond funds.

The municipal bond market is vast, with over $4 trillion in outstanding debt. Tokenization aims to modernize this infrastructure by reducing settlement times from days to minutes and enabling smaller investors to participate in high-quality credit. However, the core value proposition remains the same: stable, tax-advantaged income backed by the taxing power or revenue streams of local governments.

Onchain credit strategy and liquidity

Tokenizing municipal bonds shifts the asset from a static holding to an active liquidity instrument. For the investor, this transition unlocks three structural advantages that traditional bond markets struggle to match: fractional ownership, continuous settlement windows, and programmable yield distribution.

Fractional ownership and capital efficiency

Traditional municipal bonds often have minimum denominations of $5,000 or $10,000, creating a barrier for smaller investors and limiting portfolio diversification. Onchain tokenization breaks these bonds into smaller, tradable units. This fractionalization allows investors to allocate capital precisely, spreading risk across multiple issuers or bond tranches without tying up large amounts of liquidity in single positions.

24/7 settlement and trade execution

The traditional bond market operates on T+1 or T+2 settlement cycles, with strict business-hour constraints. Onchain markets operate continuously. While regulatory frameworks like the SEC’s proposed sandbox for tokenized municipal instruments are still evolving to handle cross-ledger exchanges, the underlying infrastructure enables near-instant settlement. This reduces counterparty risk and frees up capital that would otherwise be trapped in the clearing process.

Programmable yield distribution

Smart contracts automate the distribution of interest payments. Instead of waiting for manual processing by trustees or paying agents, yield is distributed directly to token holders’ wallets according to predefined rules. This transparency reduces administrative overhead and ensures that income streams are reliable and auditable on-chain. For investors, this means a more predictable and efficient cash flow model.

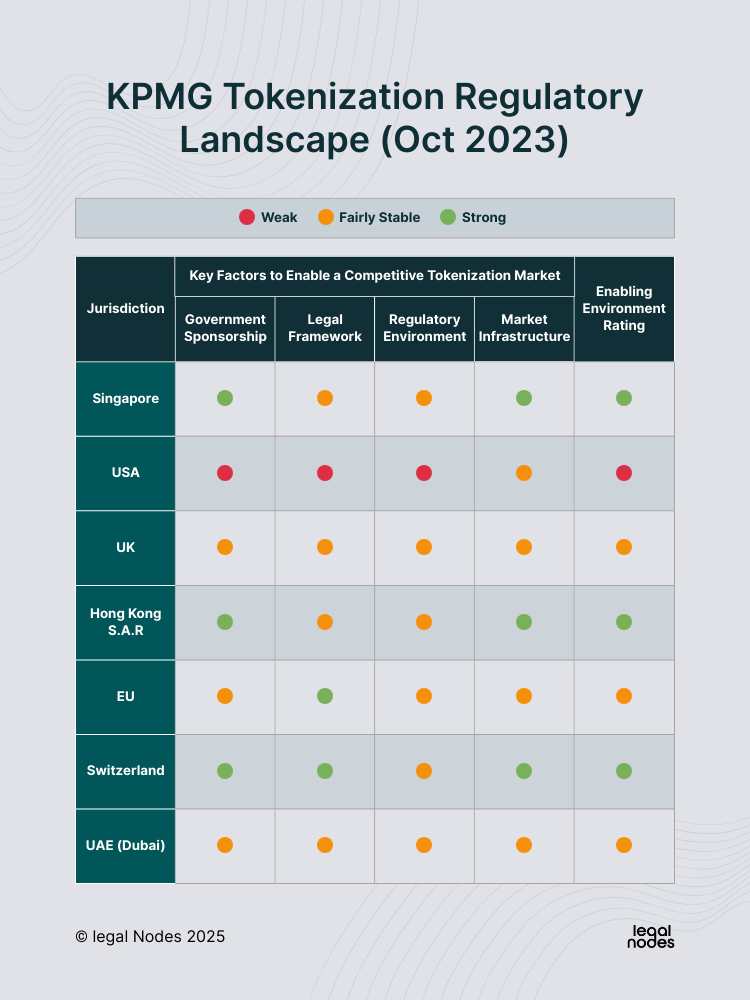

Regulatory oversight and compliance

Tokenized municipal bonds operate at the intersection of traditional finance and distributed ledger technology, meaning they must satisfy the same rigorous oversight as their paper counterparts. The U.S. Securities and Exchange Commission (SEC) has moved from theoretical guidance to active experimentation, establishing a regulatory sandbox framework to test how tokenized securities can coexist with existing market structures. This sandbox allows issuers and market participants to trial tokenized instruments under controlled conditions, ensuring that investor protections remain intact as the technology matures.

The primary challenge in this space is interoperability and compliance across different blockchain networks. The SEC’s recent framework documents highlight specific scenarios, such as an investor wishing to exchange one tokenized municipal bond for another, where the underlying securities may exist on separate distributed ledgers. Resolving these cross-chain transactions requires robust compliance protocols that can verify ownership, track beneficial owners, and ensure that every transfer adheres to federal securities laws. Without standardized compliance layers, the efficiency gains of tokenization could be negated by legal ambiguity.

Beyond the sandbox, the Municipal Securities Rulemaking Board (MSRB) continues to enforce strict reporting and transparency standards. Tokenized munis are not exempt from these rules; they must maintain the same level of disclosure and trade reporting as traditional bonds. This dual-layer oversight—SEC for securities law and MSRB for municipal market conduct—creates a high-stakes environment where technical innovation must be matched by regulatory precision. Investors should view these compliance requirements not as hurdles, but as essential safeguards that preserve the credit quality and liquidity of the asset class.

Practical checklist for tokenized bond investors

Before committing capital to a tokenized US municipal bond, treat the process like a hybrid audit. You are evaluating both the traditional creditworthiness of the issuer and the technical integrity of the blockchain infrastructure. This checklist ensures you do not overlook regulatory nuances or smart contract risks.

Start with the basics. Confirm the bond’s CUSIP and check the Municipal Securities Rulemaking Board (MSRB) for official statements. Ensure the token represents a direct claim on the underlying municipal debt and not a synthetic derivative. The MSRB remains the primary source for verifying bond specifics and issuer credit profiles.

Tokenized securities are still securities. Verify that the issuer and the tokenization platform are registered with the SEC or operating under a valid exemption. The SEC has explicitly stated that tokenization does not change the regulatory status of the asset. Investing in non-compliant tokens exposes you to significant legal and liquidity risks.

Review the smart contract audit reports from reputable firms. Look for recent audits that specifically address minting, burning, and transfer restrictions. Additionally, assess the custody solution: are keys held by a qualified custodian, or is self-custody required? Understanding who controls the private keys is critical for asset recovery in case of platform failure.

Tokenization promises better liquidity, but reality varies. Check which exchanges list the token and what the average bid-ask spread is. Unlike traditional bonds, tokenized muni markets can be fragmented. Ensure you have a clear exit strategy and understand any lock-up periods or transfer restrictions imposed by the platform.

This workflow helps you assess the intersection of traditional finance and blockchain technology. By systematically verifying the asset, the regulations, the code, and the market, you can make informed decisions about tokenized municipal bonds.

Frequently asked questions about tokenized munis

Can you tokenize bonds?

Yes. It is possible to tokenize any type of security, including stocks, bonds, notes, investment contracts, options on securities, and security-based swaps, according to the SEC.

How does tokenization work for munis?

Tokenization converts a bond into a digital token on a blockchain. Smart contracts automate execution, such as interest payments and maturity, replacing manual processes with code.

Are tokenized munis regulated?

Yes. Tokenized securities remain subject to federal and state securities laws. The SEC and MSRB oversee compliance, ensuring investor protection and market integrity.

What are the benefits of tokenization?

Tokenization offers 24/7 trading, faster settlement, and lower costs. It increases liquidity for traditionally illiquid municipal bonds.

Is tokenization safe?

Security depends on the blockchain and smart contract design. Reputable platforms use audited code and comply with regulatory standards to mitigate risks.

No comments yet. Be the first to share your thoughts!