Tokenized US municipal bonds: the practical reality

The concept of tokenized US municipal bonds is no longer theoretical. In 2024, the city of Miami issued $10 million in tax-exempt bonds using blockchain technology, marking the first transaction of its kind in the United States [[src-serp-2]]. This milestone proves that the infrastructure for onchain credit exists today, not just in labs or pilot programs.

However, the market remains in its early stages. Traditional municipal bonds often come with high minimum denominations—typically $5,000, but frequently $100,000 or more for institutional deals. This high barrier narrows the investor base and reduces liquidity. Tokenization aims to break these bonds into smaller, fractional units, potentially expanding the pool of potential investors and increasing market depth [[src-serp-1]].

While the technology is ready, regulatory clarity and widespread adoption are still evolving. The Securities and Exchange Commission has confirmed that tokenizing securities, including bonds, is possible, but it requires strict adherence to existing securities laws [[src-serp-2]]. For now, tokenized munis are a niche product, primarily available to qualified investors through specialized platforms rather than mainstream retail exchanges.

Tokenized us municipal bonds choices that change the plan

Tokenized US municipal bonds promise to modernize a market that has long relied on paper-heavy settlement and high minimums. Traditional muni bonds often carry denominations of $5,000 to $100,000, which narrows the pool of potential investors and keeps liquidity thin. On-chain tokenization can split these large obligations into smaller, fractional shares, potentially opening the asset class to retail and smaller institutional players.

However, this shift introduces specific tradeoffs that investors must weigh against traditional off-chain holdings. The primary value lies in efficiency and access, but it comes with regulatory uncertainty and platform risk. Before allocating capital, you should evaluate how liquidity, compliance, and technology stack up against the stability of the traditional bond market.

Key Evaluation Factors

The transition from physical certificates to digital tokens changes how you interact with the asset. Below is a comparison of the core tradeoffs between traditional municipal bonds and their tokenized counterparts.

| Factor | Traditional Muni | Tokenized Muni | Investor Impact |

|---|---|---|---|

| Minimum Investment | $5,000–$100,000 | Often <$100 | Lower barrier to entry for retail investors |

| Settlement Time | T+2 days | Near-instant (T+0) | Faster capital recycling and reduced counterparty risk |

| Liquidity | Low (OTC market) | Potentially Higher (24/7 trading) | Improved ability to exit positions quickly |

| Compliance | Standard KYC/AML | Embedded/Smart Contract | Automated restrictions but smart contract risk |

| Regulatory Status | Established | Evolving Sandbox/Pilot | Higher regulatory uncertainty and legal ambiguity |

The table above highlights that while tokenization offers superior speed and accessibility, it currently operates in a less mature regulatory environment. Traditional bonds benefit from decades of legal precedent, whereas tokenized instruments are often still in pilot programs or regulatory sandboxes, such as those explored by the SEC.

Market Context and Tools

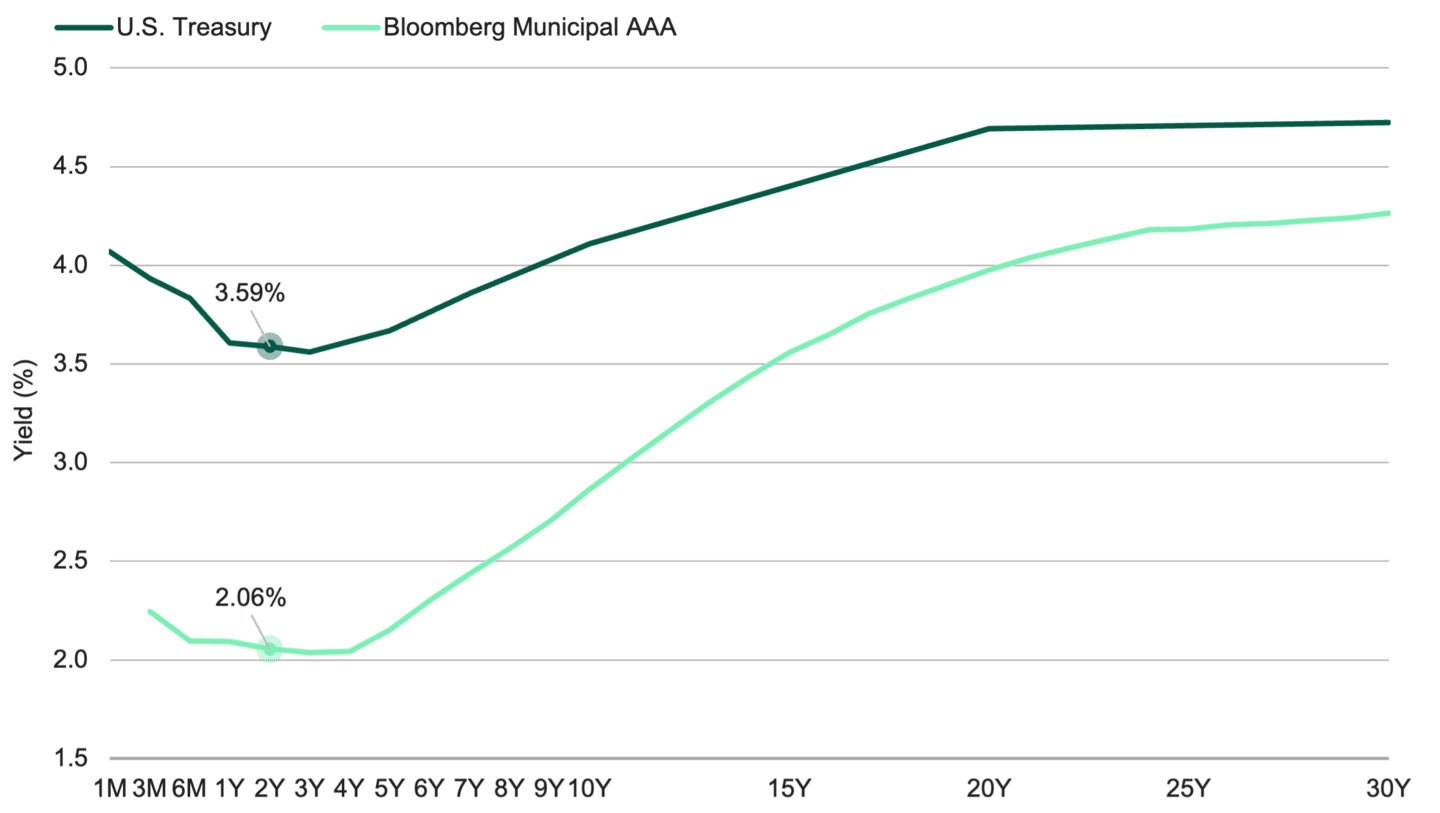

To understand the broader market dynamics, it is helpful to look at current municipal bond performance. The traditional muni market remains substantial, with SIFMA reporting over $300 billion in recent trading volumes. Tokenized assets are a tiny fraction of this total but are growing as major financial institutions test blockchain infrastructure.

For investors analyzing the broader credit market, monitoring traditional benchmarks provides context for tokenized yields. The chart below shows the recent performance of a major municipal bond ETF, which serves as a proxy for the underlying asset class.

When evaluating specific tokenized platforms, consider the following practical checks:

- Issuer Adoption: Has the municipality or issuer officially partnered with a blockchain provider? Early adopters like the City of Philadelphia have issued digital bonds, providing real-world proof of concept.

- Secondary Market Access: Does the platform offer a regulated secondary market? Without a way to sell, the "liquidity" benefit is theoretical.

- Custody Solutions: Who holds the underlying legal claim? Ensure the token is backed by a reputable custodian that maintains the traditional bond record alongside the digital token.

- Regulatory Compliance: Does the platform adhere to current securities laws? Look for platforms operating within recognized regulatory frameworks or sandboxes to mitigate legal risk.

How to Choose a Tokenized Municipal Bond Strategy

Tokenizing municipal bonds shifts the market from high-denomination institutional assets to accessible, liquid onchain instruments. With cities like those in Pennsylvania exploring blockchain issuance, the infrastructure is maturing. However, the market is not a single product; it is a set of tools for different goals. Use the framework below to match your capital size and liquidity needs to the right tokenized bond vehicle.

Traditional munis often carry $5,000 to $100,000 minimums, locking capital for years. Tokenization breaks these into smaller units, allowing you to enter and exit positions faster. If you need flexible access to your funds, prioritize platforms that offer secondary market trading for tokenized bonds rather than holding to maturity. This liquidity premium often comes with a slight yield discount compared to traditional buy-and-hold strategies.

Tokenized bond platforms charge issuance, custody, and transaction fees that vary significantly. A high yield on paper may disappear after platform fees. Look for platforms that provide transparent fee structures and offer yields that exceed traditional muni funds after costs. Compare the net yield against the convenience of fractional ownership and automated tax reporting capabilities.

Not all tokenized bonds are created equal. Some are backed by general obligation bonds, while others are revenue-backed from specific projects. Check the underlying issuer’s credit rating and the specific project details. Platforms that provide real-time access to bond covenants and issuer financials offer a clearer risk profile than opaque wrappers.

As an Amazon Associate, we may earn from qualifying purchases.

Watch out for weak tokenized bond options

The promise of tokenized municipal bonds is liquidity, but the current market is still fragmented. Many platforms offer access to onchain credit, but the underlying mechanics vary wildly. Some are merely digital wrappers around traditional custodians, while others attempt true on-chain settlement. The difference matters for both yield and risk.

Be wary of platforms claiming full decentralization for tax-exempt debt. Most current issuances, like the recent $10 million transaction by a US city, still rely on hybrid models where legal structures sit off-chain. If a platform cannot clearly explain how the legal bond deed maps to the token, treat it as a high-risk wrapper rather than a direct investment vehicle.

Another common mistake is ignoring the secondary market depth. Tokenization does not automatically create buyers. Without a robust network of institutional counterparties, your "liquid" token may be impossible to sell without a massive discount. Always check the trading volume and the specific exchange or DEX where the token settles before committing capital.

Finally, verify the issuer's technical maturity. Not all municipalities have the infrastructure to manage blockchain-based distributions. A platform might look attractive, but if the issuer defaults on the technical side—failing to distribute interest payments to wallet addresses—the token becomes worthless regardless of the underlying asset's quality.

No comments yet. Be the first to share your thoughts!