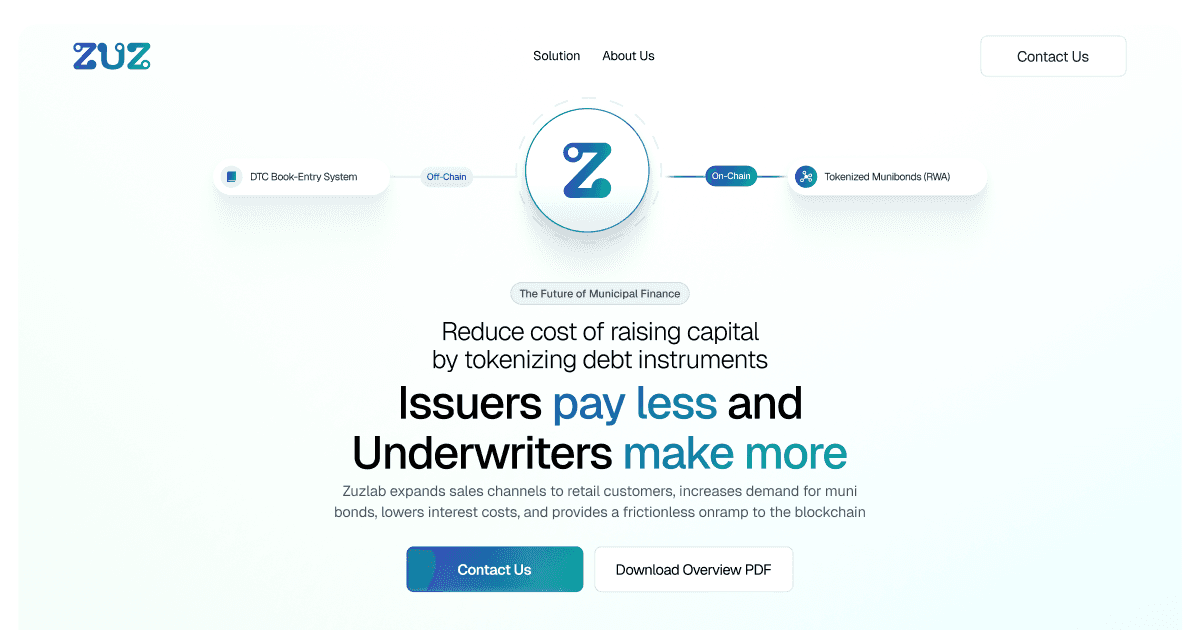

What tokenized munis actually are

Tokenized municipal bonds are not a new asset class. They are a digital wrapper around existing debt. When a municipal bond is tokenized, the ownership, transfer rights, and economic terms of that bond are encoded into a digital token that lives on a blockchain. The underlying asset remains the same: a debt security issued by states, cities, counties, or other governmental entities to fund day-to-day obligations or capital projects.

Think of it like converting a paper check into a digital payment. The value and the obligation don't change; only the method of holding and moving them does. Traditional munis rely on custodians, clearinghouses, and settlement cycles that can take days. Tokenization moves these records onto a distributed ledger, allowing for near-instant settlement and 24/7 trading potential.

This distinction matters because it clarifies the risk profile. You are still exposed to the creditworthiness of the issuer and the interest rate environment. You are not buying a speculative crypto derivative; you are buying a tokenized version of a fixed-income instrument. As Fidelity notes, this is an evolution of infrastructure, not a revolution of the asset itself.

The primary benefit is operational efficiency. By encoding the bond's legal and economic terms directly into the token, issuers and investors can automate coupon payments, reduce administrative overhead, and potentially unlock liquidity that was previously locked up in slow settlement processes.

How the onchain infrastructure works

Tokenized municipal bonds rely on smart contracts to replace traditional intermediaries. A smart contract is software stored on a blockchain that automates the execution of agreements. When you buy a tokenized bond, the contract records your ownership and handles transfer rights without needing a central clearinghouse.

The SEC’s pilot program structures these tokens as digital representations of traditional municipal debt. This means the underlying asset remains a standard municipal bond, but its lifecycle is managed on-chain. Smart contracts automate routine tasks like interest payments and maturity redemptions, reducing the friction of manual processing.

This infrastructure shifts trust from institutions to code. By automating the agreement, the system minimizes the risk of human error or delay. However, it introduces new technical risks, such as smart contract vulnerabilities, which require rigorous auditing.

Regulatory sandbox and SEC pilot updates

The Securities and Exchange Commission has moved beyond theoretical discussions on tokenized assets. It is now testing how digital representations of traditional municipal debt instruments function within a controlled environment. This isn't a free-for-all; it is a supervised pilot designed to validate infrastructure before broader adoption.

The framework treats tokenized securities as digital twins of existing bonds. The goal is to see if blockchain can streamline settlement and custody without introducing unmanageable risks. By keeping the underlying asset identical to traditional municipal debt, regulators can isolate the technology's impact on market efficiency.

Official SourceThis approach aligns with broader market modernization efforts. The SEC is looking for concrete data on how these instruments behave under stress, not just how they perform in ideal conditions. Participants must adhere to strict reporting standards, ensuring that every transaction is traceable and compliant with existing securities laws.

For investors, this signals a cautious but serious commitment to onchain infrastructure. The pilot provides a glimpse into a future where municipal bonds might settle in minutes rather than days. Until the framework expands, however, participation remains limited to approved entities operating under direct regulatory supervision.

Tokenized vs traditional muni bonds

The shift from paper to onchain infrastructure changes more than just where you hold your assets; it alters the mechanics of how those assets move. Traditional municipal bonds rely on a legacy chain of intermediaries, while tokenized versions attempt to compress that chain using distributed ledger technology. Understanding the difference is essential for evaluating whether the efficiency gains justify the structural changes.

Settlement and Liquidity

In the traditional market, buying a municipal bond typically involves T+2 settlement, meaning two business days after the trade date. During this window, your capital is tied up, and the trade is not yet final. This delay is managed by custodians and clearinghouses, adding layers of administrative overhead. Tokenized bonds, by contrast, can enable near-instant settlement. When the blockchain records the transfer, ownership changes immediately, removing the settlement risk that exists during the two-day window.

Liquidity follows a similar divergence. Traditional munis trade over-the-counter (OTC), often with wide bid-ask spreads and limited visibility. You might hold a bond for years before finding a buyer. Tokenization can unlock secondary market liquidity by allowing fractional ownership and 24/7 trading on digital platforms. This doesn't mean every tokenized bond will trade daily, but the potential for liquidity is structurally higher because the barrier to entry is lower and the transfer mechanism is faster.

Costs and Intermediaries

The traditional model is expensive because it is labor-intensive. Every transfer requires reconciliation between banks, brokers, and custodians. Each entity charges a fee for its role in the chain. Tokenization reduces the need for these intermediaries. Smart contracts can automate interest payments and principal returns, reducing the operational costs associated with manual processing.

However, "lower cost" doesn't always mean "lower fees" for the end investor. While transaction fees on-chain might be small, the cost of accessing these platforms often comes from management fees or platform subscriptions. Traditional brokers may charge commission-free trades on munis, but the spread often hides the cost. Tokenized platforms may charge explicit fees for onboarding and trading. It is crucial to look at the total cost of ownership, not just the headline fee.

Comparison Overview

The table below summarizes the key structural differences. Note that tokenized muni markets are still emerging, so liquidity and access vary significantly by platform and issuer.

| Feature | Traditional Muni Bonds | Tokenized Muni Bonds |

|---|---|---|

| Settlement | T+2 (2 business days) | Near-instant (T+0) |

| Minimum Investment | Often $5,000+ per bond | Can be fractional ($10+) |

| Trading Hours | Market hours only | 24/7 potential |

| Intermediaries | Multiple (custodians, brokers) | Reduced (smart contracts) |

| Liquidity | Low (OTC market) | Variable (platform-dependent) |

| Transparency | Limited (MSRB reports post-trade) |

Market strategy and investment considerations

Tokenized municipal bonds offer a way to improve portfolio efficiency by bringing onchain liquidity to a traditionally illiquid market. The strategy hinges on reducing the friction between trade execution and settlement, which can generate incremental alpha for active managers. By automating interest payments and reducing back-office overhead, these assets allow investors to access segments that were previously too costly to touch.

The strategic advantage lies in the speed of settlement. Traditional muni trades often settle days after execution, tying up capital. Onchain infrastructure can compress this timeline, freeing up cash for redeployment. This efficiency is particularly valuable in volatile markets where timing is critical. However, this speed also means that errors or smart contract vulnerabilities can be exploited instantly, raising the stakes for due diligence.

Early adoption is high-risk. While the potential for alpha is real, the infrastructure is still maturing. Investors must weigh the benefits of liquidity and efficiency against the technical risks of blockchain integration. It is not a passive strategy; it requires a deeper understanding of both fixed-income mechanics and digital asset custody. As the market matures, the gap between traditional and tokenized munis may narrow, but for now, the edge comes from navigating the complexity.

-

Verify smart contract audits and security history

-

Confirm tax treatment of onchain interest payments

-

Assess liquidity depth and trading volume

-

Understand custody solutions and private key management

No comments yet. Be the first to share your thoughts!