What tokenized muni bonds actually are

Tokenized US Municipal Bonds works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

The traditional muni market structure

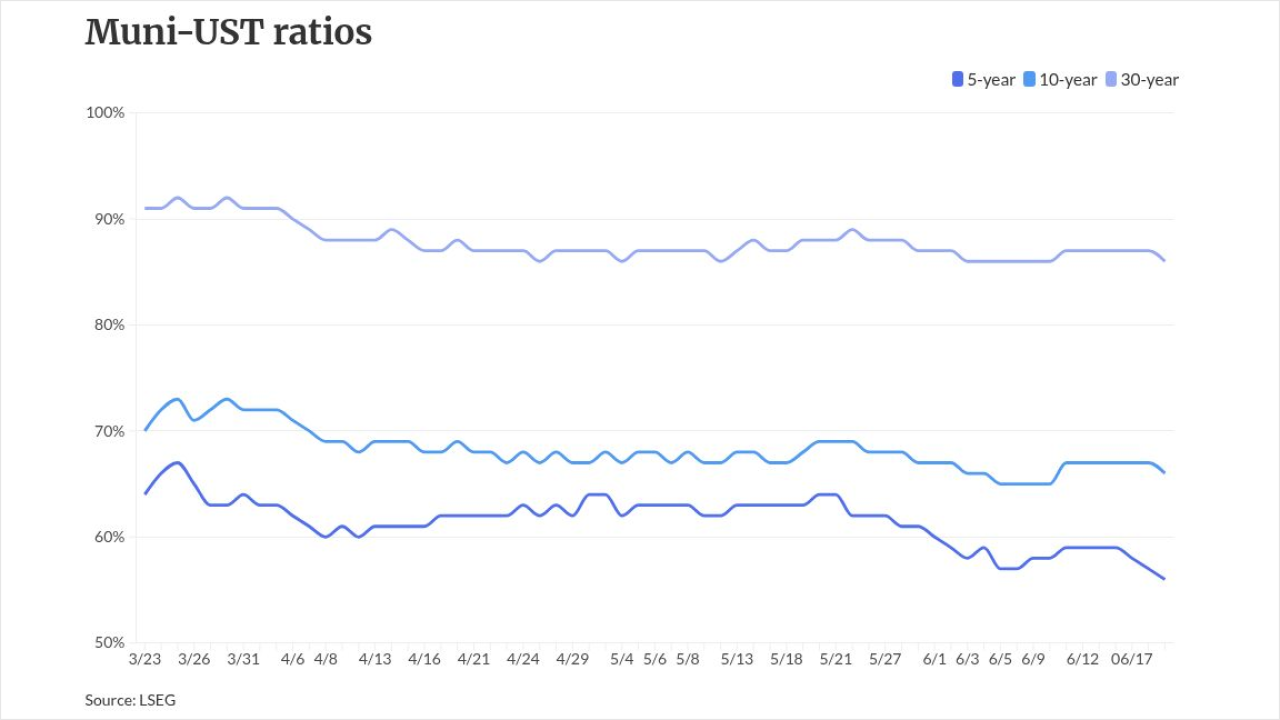

The US municipal bond market is a massive, $4 trillion+ ecosystem that serves as the backbone of local infrastructure. From schools and hospitals to water systems and roads, these bonds fund essential public services. Yet, for most individual investors, this market remains largely out of reach. It is a world defined by fragmentation, high barriers to entry, and opaque pricing structures that favor institutional players.

At its core, the traditional muni market operates over-the-counter (OTC). Unlike stocks traded on centralized exchanges, municipal bonds are bought and sold through a decentralized network of dealers. This structure creates significant inefficiencies. According to SIFMA, while the market is deep, trading is often thin for individual issues, leading to wide bid-ask spreads. Investors rarely see the full picture of liquidity, making it difficult to execute trades at fair value without the help of a broker-dealer.

This fragmentation is compounded by high minimum investment requirements. Historically, a single municipal bond issue might require an initial investment of $5,000 to $100,000 or more. This barrier effectively excludes retail investors from direct ownership, forcing them into municipal bond mutual funds or ETFs to gain exposure. While these funds provide diversification, they come with management fees and lack the tax advantages of holding individual bonds to maturity.

The result is a market that is both critical and inaccessible. The inefficiencies and high minimums create a friction point that tokenization aims to solve. By breaking bonds into smaller, digital units, tokenized US municipal bonds can democratize access, improve liquidity, and streamline settlement. Understanding this traditional structure is the first step in seeing how blockchain technology can reshape such a foundational asset class.

To visualize the broader trends in the municipal bond market, it helps to look at the performance of major municipal bond ETFs. The iShares National Muni Bond ETF (MUB) is a key benchmark for the sector, reflecting the health and interest rate sensitivity of the broader market.

The Rails Behind Tokenized Municipal Bonds

Before tokenized US municipal bonds move from pilot to permanent fixture, they need more than just blockchain code. They require a clear regulatory path and a network of trusted intermediaries to handle the messy parts of finance that smart contracts can’t yet automate. Think of the blockchain as the track and the traditional financial infrastructure as the train; both must align for the journey to work.

The SEC Regulatory Sandbox

The Securities and Exchange Commission (SEC) is currently exploring a "regulatory sandbox" to test these innovations safely. According to their November 2025 proposal, this framework would allow participating municipalities to issue tokenized versions of traditional bonds within a controlled environment. This isn’t about bypassing rules, but rather testing them under supervision to ensure investor protection remains intact.

The sandbox approach aims to reduce uncertainty for issuers and investors alike. By operating within defined boundaries, municipalities can experiment with fractional ownership and faster settlement times without risking systemic stability. The SEC’s goal is to modernize market infrastructure while keeping the core tenets of securities law—transparency and fairness—firmly in place.

The Role of Regulated Intermediaries

Blockchain doesn’t replace the existing financial plumbing; it upgrades it. Regulated intermediaries like transfer agents, clearinghouses, and custodians remain essential. They handle the legal verification of bondholders, manage tax withholding, and ensure that token transfers comply with federal and state securities laws.

For example, the Municipal Securities Rulemaking Board (MSRB) continues to set reporting and trading standards that apply regardless of whether a bond is held in physical form or as a digital token. These entities act as the bridge between the digital ledger and the real world, ensuring that a token representing a bond is backed by a legitimate legal claim. Without this layer of regulated oversight, the market for tokenized US municipal bonds would lack the trust required for large-scale adoption.

Why Infrastructure Matters

The high costs associated with traditional bond issuance often result in minimum denominations of $5,000 or even $100,000. This narrows the market and excludes smaller investors. Tokenization aims to break these barriers by enabling fractional ownership, effectively expanding the potential investor base. However, this expansion only works if the underlying infrastructure is robust.

The combination of a supportive regulatory sandbox and reliable intermediaries creates the foundation for a more inclusive municipal bond market. It’s not just about technology; it’s about building a system that is both innovative and compliant. As the SEC continues to refine its sandbox proposals, the focus remains on creating a seamless, secure, and efficient market for the next generation of municipal debt.

How to access onchain credit exposure

Investors looking into the tokenized us municipal bonds market research are essentially choosing between two distinct plumbing systems for the same underlying asset. On one side, you have the familiar, regulated ecosystem of traditional exchange-traded funds. On the other, a newer, blockchain-native infrastructure that promises greater efficiency but carries different operational risks. Understanding the mechanics of each is necessary before allocating capital.

The traditional ETF route

The most common entry point remains the municipal bond ETF. These funds pool capital to buy baskets of tax-exempt bonds, offering instant diversification and daily liquidity. For most retail investors, this is the default choice because it integrates seamlessly with existing brokerage accounts. The primary trade-off is the management fee and the fact that you own a share of a fund, not the underlying bond itself.

To understand the baseline performance of this traditional vehicle, it helps to look at live market data for a major fund like the iShares National Muni Bond ETF (MUB). This provides a reference point for yield and volatility against which newer tokenized products are often measured.

The tokenized bond alternative

Tokenized municipal bonds represent a shift toward direct ownership. Instead of buying a fund share, you purchase a digital token that represents a claim on the underlying bond. This model can reduce intermediaries, potentially lowering costs and speeding up settlement. However, the infrastructure is still maturing. Liquidity pools may be thinner than ETFs, and the technology stack introduces new cybersecurity and compliance considerations that traditional finance does not face.

Side-by-side comparison

The choice isn't just about yield; it's about how you want to interact with the asset. The table below breaks down the structural differences in liquidity, entry barriers, and settlement mechanics.

| Feature | Traditional Muni ETF | Tokenized Muni Bond |

|---|---|---|

| Liquidity | High (daily market trading) | Variable (depends on DEX/OTC) |

| Minimum Investment | Price of one share (~$100) | Often fractional (e.g., $10) |

| Settlement Speed | T+1 or T+2 | Near-instant (blockchain finality) |

| Intermediaries | Reduced (smart contracts) | |

| Regulatory Oversight | SEC, SIFMA standards | Evolving (SEC, state laws) |

Strategic considerations

While tokenization offers technical advantages in speed and accessibility, it does not eliminate credit risk. The underlying municipal bonds still carry the same default probabilities as their traditional counterparts. The difference lies in operational risk. With tokenized assets, you must trust the digital infrastructure, the wallet security, and the regulatory framework surrounding digital securities. Traditional ETFs offer a layer of institutional protection that is currently more standardized.

Before committing funds to either channel, verify that the tokenized product you are considering is fully compliant with SEC regulations and backed by a licensed custodian. The infrastructure is promising, but due diligence remains the most critical part of the strategy.

No comments yet. Be the first to share your thoughts!