What tokenized muni bonds actually are

Tokenized municipal bonds are not a new type of debt. They are traditional municipal bonds represented as digital tokens on a blockchain. When you hold a tokenized muni, you hold the same legal claim to interest payments and principal repayment as you would with a paper certificate or a DTC deposit.

The difference lies in settlement and custody. Traditional munis settle via the Depository Trust Company (DTC) and involve paper trails, clearinghouses, and multi-day settlement cycles. Tokenization encodes ownership, transfer rights, and economic terms into a smart contract. This allows for near-instant settlement and 24/7 trading on secondary markets, removing the friction of traditional intermediaries.

It is important to distinguish this from stablecoins or cryptocurrency. A tokenized muni is a security, not a currency. Its value is tied to the creditworthiness of the municipal issuer—such as a city school district or water authority—not to a fiat peg or speculative algorithm. You are still lending money to a government entity in exchange for a promise of regular interest payments and the return of face value, as defined by the Municipal Securities Rulemaking Board (MSRB).

This shift creates "onchain credit," where the legal and economic terms of the bond are self-executing. Smart contracts can automatically distribute coupon payments to token holders and enforce maturity dates without manual intervention. This reduces operational risk and counterparty exposure, making the bond more efficient to manage for both issuers and investors.

Verify regulatory compliance

Tokenized US municipal bonds sit at the intersection of traditional fixed-income securities and emerging blockchain technology. Before committing capital, you must confirm that the specific instrument complies with current SEC guidelines and state-level securities laws. The regulatory environment is still evolving, so relying on a platform that operates within an official regulatory sandbox is the safest starting point.

Check issuer registration and smart contract audits

Legitimate tokenized munis are issued by registered entities that adhere to the same disclosure standards as traditional bonds. You should verify that the issuer is registered with the Municipal Securities Rulemaking Board (MSRB) and that the underlying assets are clearly defined. Equally important is the technical layer: the smart contract governing the token must have undergone a third-party security audit. This audit confirms that the code automating coupon payments and maturity dates functions exactly as written, without exploitable vulnerabilities.

Confirm SEC sandbox participation

The Securities and Exchange Commission (SEC) has proposed a regulatory sandbox framework specifically for tokenized municipal instruments. This sandbox allows for time-limited testing of issuance and settlement processes under regulatory supervision. When evaluating a tokenized muni, look for explicit confirmation that the platform or issuer is participating in or authorized by such a framework. This oversight provides a layer of protection that purely decentralized, unregulated crypto-assets do not offer. Without this regulatory anchor, the investment carries significantly higher legal and operational risk.

Confirm the issuer is registered with the MSRB and that the bond terms are publicly disclosed. This ensures the underlying asset is a legitimate municipal security, not a speculative wrapper.

Locate the most recent third-party security audit for the token’s smart contract. The report should verify that the code correctly automates interest payments and principal repayment without errors.

Check if the platform operates within an SEC regulatory sandbox. This framework provides supervised testing of tokenized securities, offering a higher degree of legal certainty than unregulated DeFi protocols.

Step two: Choose a qualified onchain platform

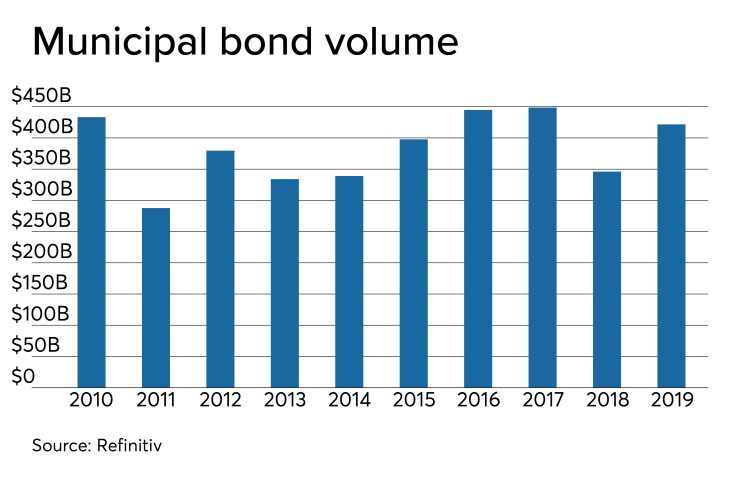

Tokenized US Municipal Bonds works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Execute the purchase and settlement

This section covers the final transaction mechanics of buying tokenized US municipal bonds. We walk through connecting to a compliant platform, verifying identity, placing the order, and understanding on-chain settlement. The process mirrors traditional bond trading but settles on a blockchain ledger.

Link a self-custody wallet or a platform-managed account to the tokenized bond marketplace. Ensure the wallet supports the specific blockchain network (e.g., Ethereum, Polygon) where the bond tokens reside. This step establishes the secure digital identity required for all subsequent transactions.

Undergo Know Your Customer (KYC) and Anti-Money Laundering (AML) verification. Tokenized bonds are regulated securities, so platforms require identity confirmation before allowing purchases. This process ensures compliance with SEC and MSRB regulations, preventing unauthorized access to municipal debt instruments.

Select the specific municipal bond, choose the quantity, and submit your order. The platform matches your buy request with available supply or executes it via an internal ledger. Unlike traditional markets, this step often occurs in real-time without the typical T+2 settlement delay, though final on-chain settlement may follow shortly after.

Once the trade is confirmed, the smart contract mints or transfers the bond tokens to your wallet. These ERC-20 or ERC-1400 tokens represent your legal ownership of the municipal bond. The blockchain ledger now permanently records your holding, replacing the traditional paper or central depository record.

Smart contracts automate coupon payments directly to your wallet. When interest dates arrive, the issuer’s smart contract distributes payments in stablecoins or fiat-pegged tokens without manual intervention. This eliminates the need for intermediary banks to process payments, reducing fees and settlement risk for investors.

By following these steps, you transition from traditional bond ownership to a fully digital, automated experience. The blockchain handles the heavy lifting of record-keeping and payment distribution, while you retain full custody of your asset.

Manage yield and tax reporting

Tokenized municipal bonds work like traditional munis: you lend money to a city or state and receive regular interest payments until the bond matures. The difference is that these payments come through smart contracts on a blockchain, which automates distribution and reduces administrative friction. You still need to track your yield, but the reporting mechanics change slightly depending on how the platform handles tax documents.

First, understand the yield structure. Most tokenized munis pay interest semi-annually, just like their traditional counterparts. The yield is calculated based on the bond’s coupon rate and your purchase price. Because blockchain transactions are immutable, you can verify every payment directly on the ledger. This transparency makes it easier to reconcile your income without waiting for quarterly statements from a custodian.

Tax reporting requirements

Tax reporting for tokenized bonds is still evolving, but the underlying obligations remain the same. Interest from most municipal bonds is exempt from federal income tax and, in many cases, state and local taxes if you live in the issuing state. When you receive interest payments, the platform should provide a tax document equivalent to the traditional Form 1099-INT.

Checklist:

- Verify the platform’s tax document generation process before investing.

- Confirm whether the bond is federally tax-exempt and, if so, which states are exempt.

- Keep records of all on-chain transactions for potential AMT (Alternative Minimum Tax) reporting.

- Consult a tax professional about the crypto-tax implications of holding digital securities.

If the platform does not automatically generate tax forms, you will need to manually report your interest income. This adds a layer of administrative work that traditional brokerages typically handle for you. Always prioritize platforms that integrate with established tax reporting services to avoid compliance headaches.

State-specific exemptions

Not all municipal bonds are created equal when it comes to taxes. Interest from bonds issued by your home state is usually exempt from both federal and state income taxes. Bonds issued by other states are generally only exempt from federal tax. Some municipalities also offer tax-exempt status for bonds issued within specific counties or school districts.

Before investing, check the bond’s prospectus or the issuer’s official statement to confirm the tax status. This information is critical for calculating your after-tax yield. A bond with a higher coupon rate might actually yield less than a lower-rate bond if it lacks favorable tax exemptions.

Crypto-tax implications

Holding bonds as digital tokens introduces unique tax considerations. In the U.S., the IRS treats cryptocurrencies as property, which means you may face capital gains tax when you sell or exchange your tokenized bonds. However, the interest payments themselves are generally treated as ordinary income, similar to traditional bonds.

If you trade tokenized bonds on a secondary market, each sale is a taxable event. You must track your cost basis for each token lot to calculate gains or losses accurately. Blockchain explorers can help you verify transaction histories, but you will need to reconcile this data with your tax software. Keep detailed records of every transaction to simplify year-end reporting.

Common Tokenized Muni Mistakes

Tokenized municipal bonds offer efficiency, but they introduce technical risks that traditional bondholders rarely face. You must understand these specific pitfalls before allocating capital. The SEC’s sandbox framework for tokenized municipal instruments highlights how regulatory structures are still evolving, meaning compliance isn't always as straightforward as with legacy securities.

Ignoring Smart Contract Risk

In tokenized munis, your legal claim is enforced by code, not just a prospectus. If the smart contract has a vulnerability, your principal is exposed. Unlike a paper bond held in DTC, you cannot easily reverse a transaction if the underlying code fails. Always verify that the contract has undergone third-party audits before investing.

Underestimating Liquidity Mismatches

Tokenization promises 24/7 trading, but liquidity is not guaranteed. Many tokenized muni platforms are early-stage and may lack deep order books. You might find yourself unable to sell when you need to, especially during market stress. Treat tokenized liquidity as a potential benefit, not a certainty.

Overlooking Regulatory Shifts

The regulatory landscape for digital assets is fluid. The SEC and MSRB are actively shaping how tokenized securities are issued and settled. A rule change today could impact the tax treatment or transferability of your tokens. Stay informed on official guidance from the SEC and MSRB rather than relying on platform assumptions.

No comments yet. Be the first to share your thoughts!